Why Americans Are Still Spending: A Deep Dive Into Current Consumer Trends

The Resilience of American Consumer Spending For months, analysts and economists have been bracing for a cooling effect in the retail sector,…

For generations, the transition into adulthood was marked by a clear, linear progression: graduate, find stable employment, move out, and achieve financial self-sufficiency. However, that traditional roadmap is increasingly disconnected from the modern economic reality. Today, 42% of adults rely on their parents for some form of financial assistance, a statistic that reflects a profound structural shift rather than a lack of ambition or individual failure. This trend is not an anomaly born of personal shortcomings; instead, it is a calculated, necessary response to a landscape defined by systemic economic pressures that have made the milestones of previous decades exponentially more difficult to reach.

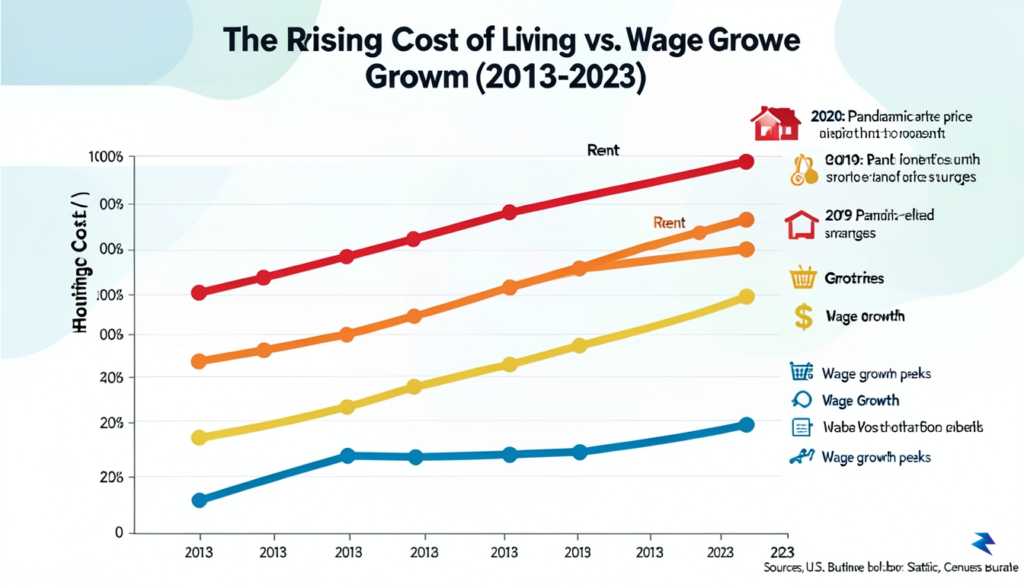

The primary driver behind this shift is the relentless escalation of the cost of living, which has significantly outpaced wage growth for the average worker. When we examine the housing market, for instance, we see a environment where entry-level homeownership has become a distant dream for many, while rental costs consume an increasingly unsustainable portion of monthly income. This squeeze is exacerbated by the crushing weight of student loan debt, which acts as a massive anchor on the financial mobility of young professionals. By the time many adults enter the workforce, they are already navigating a deficit that makes saving for a down payment or emergency fund nearly impossible without a generational safety net.

Beyond these specific hurdles, we are witnessing a broader transformation in how families view financial stability. In an era of economic volatility, the traditional “go-it-alone” model of adulthood is being replaced by a model of intergenerational interdependence. This isn’t just about paying rent; it is about families pooling resources to ensure that the younger generation can survive, let alone thrive, in an expensive, hyper-competitive economy. When nearly half of the adult population relies on parental support, we must stop viewing this as a sign of arrested development and start recognizing it as a pragmatic, collective survival strategy.

Financial interdependence is the modern answer to an economic system that no longer supports the independent advancement of the individual at the same pace it once did.

Ultimately, this 42% statistic serves as a crucial starting point for a much larger conversation about the changing social contract within families. As the barriers to entry for middle-class stability remain high, the reliance on parental support is becoming a normalized, foundational element of the transition into independent life. By acknowledging these macro-economic factors, we can move away from the stigma of “failing to launch” and toward a more empathetic understanding of how families are adapting to protect the long-term well-being of their members in an uncertain financial climate.

For too long, the cultural narrative surrounding adulthood has been defined by a rigid, binary standard: you are either fully independent, or you are failing. This mindset creates a pervasive, often paralyzing stigma that equates receiving financial help from family with a lack of personal drive or professional ambition. However, many financial therapists are now challenging this outdated perspective, urging us to recognize that there are truly no “bad guys” in these scenarios. When we peel back the layers of guilt, we often find that parental support is less about an inability to function and more about the reality of an increasingly complex economic landscape. By shifting the conversation away from shame and toward a more nuanced understanding, we can alleviate the mental health burdens that often accompany these financial arrangements.

Reframing parental support as a strategic family resource—rather than a sign of dependency—can fundamentally transform your relationship with your finances and your parents. Think of it less as a “bailout” and more as a form of intergenerational capital, similar to the way families have historically pooled resources to invest in education, housing, or small business ventures. When viewed through this lens, the support becomes a collaborative strategy designed to provide stability and long-term security. This shift in mindset allows both parties to let go of the performative expectations of total self-reliance, which often do more harm than good in a world where the cost of living has outpaced wage growth for decades.

“Financial support is not a reflection of your character, but a tool for navigating a challenging economic environment. When we remove the shame, we make room for the strategy.”

The key to making these arrangements successful lies in healthy, transparent communication. Without clear boundaries and open dialogue, even the most well-intentioned financial assistance can lead to resentment or feelings of obligation that strain family bonds. It is essential to treat these interactions like a professional partnership: discuss the specific purpose of the funds, establish a timeline for the arrangement, and ensure that both sides feel heard and respected. By normalizing these conversations, you move from a place of secrecy and shame into a space of mutual support. Ultimately, when families view themselves as a unified team working toward a common goal of stability, the stigma evaporates, leaving behind a stronger, more resilient foundation for everyone involved.

The pursuit of complete independence is a deeply ingrained cultural ideal, yet the harsh arithmetic of contemporary life frequently renders that goal unattainable for a vast segment of the population. For many young and middle-aged adults, the gap between stagnating wage growth and the skyrocketing costs of essential living has created a precarious financial reality. When a single paycheck must stretch to cover rent that has outpaced inflation, groceries, utilities, and student loan interest, the margin for error effectively disappears. Consequently, parental support has evolved from a rare safety net into a structural necessity, acting as a critical buffer against the systemic pressures that make standard middle-class living increasingly elusive.

Housing remains the most significant driver of this modern interdependence, as the barrier to entry for homeownership—and even affordable renting—has reached historic highs. In many urban centers, the traditional “thirty percent” rule for housing costs is now a nostalgic memory, with many families spending half of their monthly income just to secure a roof over their heads. When housing costs consume such a disproportionate share of the budget, there is little left to absorb the volatility of unexpected expenses, such as car repairs or medical bills. This is where parents often step in, providing down-payment assistance or monthly subsidies that allow their adult children to maintain a baseline of stability that would otherwise be impossible to achieve on a single or dual-income salary.

Beyond the fundamental need for shelter, the exorbitant cost of childcare has effectively pushed many dual-income households into a state of financial reliance. For parents attempting to balance professional obligations with the needs of a growing family, the price of quality daycare often rivals a mortgage payment, forcing a difficult choice between career advancement and household solvency. When childcare is priced out of reach, grandparents often step into the role of primary caregivers, providing a form of “in-kind” financial assistance that is just as vital as direct cash transfers. This reliance is not a sign of individual failure or a lack of ambition; rather, it is a pragmatic adaptation to an economic landscape where the cost of raising the next generation is no longer supported by the standard compensation models of the past.

The reliance on family support is not a personal shortcoming; it is a rational response to an economic environment where the cost of essential services has fundamentally decoupled from the average worker’s earning power.

Ultimately, it is crucial to recognize that this trend is not confined to any single demographic. Even families who appear to be thriving by traditional standards—those with stable jobs and moderate savings—are finding that the “cushion” required to handle life’s inevitable twists and turns is thicker than ever before. When basic necessities like healthcare, education, and insurance premiums continue to climb, even a comfortable salary can feel inadequate. By acknowledging that this phenomenon is widespread and data-backed, we can move past the stigma of intergenerational support and begin to view it for what it truly is: a necessary, resilient, and collaborative strategy for navigating a complex and often unforgiving financial world.

Mixing family relationships with financial matters often creates a delicate dance, where unspoken expectations and underlying emotions can easily lead to misunderstandings and resentment. While parental support can be a vital lifeline for many adults navigating today’s economic landscape, its success hinges on establishing clear, respectful boundaries from the outset. Without transparent communication and a mutual understanding of the arrangement, the very act of giving or receiving help can inadvertently strain the emotional bonds meant to be strengthened. Therefore, proactively addressing potential pitfalls through open dialogue is not just recommended, but essential for preserving the integrity of both the financial aid and the family relationship itself.

Successful financial arrangements between family members are built on a foundation of radical transparency and realistic expectations from all parties involved. Parents should openly communicate what they are genuinely able to provide without compromising their own financial security or future plans, ensuring their generosity doesn’t inadvertently become a burden. Similarly, adult children must clearly articulate their needs, be honest about their circumstances, and maintain realistic expectations about the extent and duration of the support they can reasonably receive. This candid approach prevents assumptions from taking root and allows for an agreement that is sustainable and equitable for everyone, fostering trust instead of hidden anxieties.

To navigate these potentially sensitive waters, it’s incredibly helpful to approach the conversation with a structured mindset, treating it almost like a professional agreement, albeit with much more warmth and understanding. The very first step involves clearly defining the purpose of the financial support. Is it intended to cover essential living expenses while the adult child pursues education, bridge a temporary job loss, contribute to a down payment, or assist in launching a new business venture? Pinpointing the exact reason for the aid helps to set clear parameters and ensures both parties are aligned on the goal. Alongside purpose, establishing a timeframe is equally critical; is this support for a specific period, a one-time gift, or an ongoing arrangement with regular review points? Setting these expectations upfront prevents open-ended commitments that can lead to dependency or donor fatigue.

Beyond purpose and timeframe, the conversation must explicitly address the expectations for repayment or transition. Is the money a gift with no strings attached, a loan to be repaid, or an investment with specific conditions? If it’s a loan, discussing repayment terms—including whether interest will be charged, a specific repayment schedule, and what happens if payments are missed—is paramount. If it’s a gift intended to help an adult child get on their feet, the discussion should include how and when the child expects to become self-sufficient. Furthermore, scheduling regular check-ins allows for adjustments as circumstances change, preventing minor issues from escalating into major conflicts and ensuring the arrangement remains beneficial and respectful for everyone involved.

Crucially, financial support should never, under any circumstances, be wielded as a tool for control or manipulation within the family dynamic. When money becomes entangled with emotional leverage, it can quickly erode trust, foster resentment, and damage the core relationship far beyond the financial transaction itself. Parents offering assistance must respect their adult child’s autonomy and life choices, understanding that their support is meant to empower, not to dictate. Conversely, adult children receiving aid should not feel obligated to conform to parental wishes in exchange for financial help. Maintaining this distinction is vital for preserving mutual respect and ensuring that the assistance genuinely supports the recipient’s independence rather than hindering it.

Financial support should empower, not dictate. Respecting autonomy is key to a healthy family dynamic.

While it might feel overly formal for a family matter, formalizing the agreement in some manner can significantly reduce ambiguity and prevent future disputes. This doesn’t necessarily mean drawing up a legally binding contract with lawyers involved, but rather documenting the agreed-upon terms in writing. A simple email summarizing the purpose, amount, timeframe, repayment expectations (if any), and review schedule can serve as a valuable reference point for both parties. Having these details recorded provides clarity, acts as a reminder of what was agreed, and offers a neutral reference if misunderstandings arise, ensuring that everyone remains on the same page.

Ultimately, successfully navigating financial support within a family requires open hearts, clear heads, and a commitment to upholding the relationship above all else. By engaging in transparent conversations, setting realistic expectations, defining clear

Transitioning from a state of reliance to one of autonomy requires more than just good intentions; it demands a structured, intentional roadmap. Rather than viewing parental assistance as a permanent safety net, it is most effective when treated as a temporary bridge to long-term stability. The first step in this process is creating a transparent budget that clearly differentiates between essential living costs and discretionary spending. By mapping out exactly where your income—including the support you receive—is allocated, you can identify “leakage” in your finances and determine which expenses can be gradually offloaded as your own income grows. Establishing this level of clarity not only helps you manage your resources more effectively but also provides your parents with the peace of mind that their contributions are being used to build a foundation for your future rather than just covering recurring deficits.

Once you have a firm grasp on your spending, you must prioritize the creation of a personal emergency fund. Even a modest savings buffer can act as a circuit breaker, preventing you from needing to ask for additional “emergency” loans when unexpected expenses arise. Concurrently, focusing on aggressive debt repayment—particularly for high-interest loans—will free up significant monthly cash flow that can then be diverted toward your own living expenses. This is where career development becomes a non-negotiable pillar of your independence strategy. Investing time in upskilling, networking, or pursuing professional certifications isn’t just about personal growth; it is the most reliable mechanism for increasing your earning potential, which eventually allows you to subsidize the portions of your life previously covered by your parents.

True financial independence is rarely an overnight transformation; it is a series of incremental decisions that slowly shift the burden from your support system to your own professional output.

Finally, the most critical element of this transition is the establishment of periodic, honest reviews of the support arrangement. Set a formal “financial check-in” schedule—perhaps quarterly—to sit down with your parents and discuss your progress. These meetings should not be viewed as high-pressure interrogations, but rather as collaborative sessions to ensure the current level of support is still serving the needs of both parties. If your income has increased, discuss how you might begin taking over a specific bill or category of expense. This approach respects the financial health of your parents, who may be approaching their own retirement, while simultaneously reinforcing your own trajectory toward total self-sufficiency. By maintaining this open dialogue, you transform a potentially awkward dynamic into a partnership built on mutual respect and long-term security.

You must be logged in to post a comment.