Ripple Secures Full MiCA Compliance: A Milestone for European Crypto Payments

The Evolution of Ripple’s European Expansion Ripple’s journey toward becoming a cornerstone of the European financial ecosystem has been…

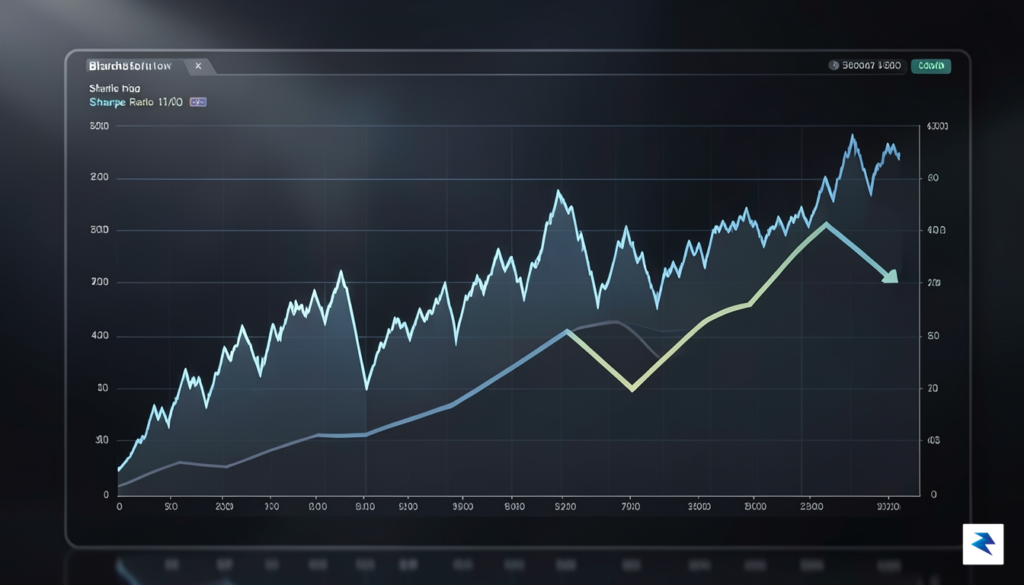

At its core, the Sharpe ratio is the financial industry’s standard way of measuring the quality of an investment’s performance. Rather than simply looking at the raw percentage gains—which can be misleading in a highly volatile environment—the Sharpe ratio adjusts those returns by accounting for the amount of risk taken to achieve them. Think of it as a “bang for your buck” metric: it tells you whether the profit you are seeing is a genuine reward for your patience or if you are simply taking on dangerous levels of volatility that could just as easily lead to a significant drawdown.

In the context of digital assets like Bitcoin, this metric becomes particularly vital because of the asset’s notorious price swings. A high Sharpe ratio suggests that an investor is being well-compensated for the turbulence they endure. Conversely, a declining ratio indicates that the volatility has become disproportionate to the gains. When the Sharpe ratio slides to multi-year lows, it serves as a warning signal that the market may be entering a phase where the “risk premium”—the extra return expected for holding a risky asset—is evaporating. Essentially, Bitcoin is becoming “expensive” in terms of risk; you are paying a higher price in volatility for every percentage point of growth you hope to capture.

To understand what constitutes a healthy level, it is helpful to establish a baseline. In traditional finance, a Sharpe ratio of 1.0 is considered good, while anything above 2.0 is often viewed as exceptional. In the wilder world of cryptocurrency, these thresholds often fluctuate, but the trend remains the primary indicator. When the ratio drops significantly, it suggests that the market is currently inefficient or exhausted, offering lower returns while maintaining high variance. Investors often use this data to decide whether to rebalance their portfolios, as a dropping ratio implies that the asset is no longer providing an attractive risk-adjusted return compared to more stable alternatives.

The Sharpe ratio is not a crystal ball for future price action, but rather a diagnostic tool that reveals whether your current strategy is working effectively within the reality of market volatility.

Ultimately, paying attention to the Sharpe ratio helps move investors beyond the “fear of missing out” or “greed” cycles that often dictate crypto markets. By focusing on risk-adjusted performance, you can objectively evaluate whether the current price of Bitcoin truly justifies the hair-raising ups and downs that characterize its daily movement. When this metric hits lows not seen since the turbulence of 2022, it is a clear call for investors to pause and reassess whether the current market climate still aligns with their personal risk tolerance and long-term financial goals.

The Sharpe ratio serves as a vital barometer for investors, measuring the excess return of an asset relative to the volatility it generates. When this metric hits levels not seen since the turbulence of 2022, it sends a clear signal that the market’s efficiency has significantly deteriorated. Currently, Bitcoin is struggling to justify its inherent risk; investors are essentially being asked to endure wider price swings for diminishing rewards. This downward trend suggests that the capital being deployed into the asset is currently facing an unfavorable risk-reward profile, as the upside potential has failed to keep pace with the ongoing noise and erratic behavior of the broader crypto ecosystem.

A primary driver of this compression is the persistent stagnation in Bitcoin’s price action. While the asset has managed to avoid a catastrophic collapse, it has simultaneously struggled to establish a definitive, high-conviction breakout that would satisfy long-term holders. When an asset spends prolonged periods moving sideways, realized volatility remains elevated because the market is constantly reacting to minor macroeconomic updates and speculative sentiment shifts. Because Bitcoin is not delivering significant upward momentum, the numerator in the Sharpe ratio calculation—the excess return—remains stubbornly low, while the denominator—the standard deviation of returns—remains disproportionately high due to these constant, jittery fluctuations.

The current market environment mirrors the structural exhaustion seen in 2022, where high volatility acted as a tax on capital efficiency rather than a catalyst for growth.

Comparing the current environment to the 2022 bear cycle reveals striking similarities in market psychology. In 2022, the ratio suffered because every attempt at a rally was swiftly met with selling pressure, leading to a “choppy” environment that punished leverage-heavy traders. Today, despite a different fundamental landscape, we see a similar inability to sustain a trend. The market is currently trapped in a regime of high-frequency oscillation, where the lack of a clear directional catalyst keeps volatility levels elevated. Consequently, for every unit of risk taken, the realized gain has been consistently eroded by these frequent, short-lived price corrections. This creates a challenging environment for institutional allocators who prioritize risk-adjusted performance, often leading them to reduce exposure until a more favorable signal-to-noise ratio emerges in the price charts.

In the current macroeconomic landscape, the traditional definition of a risk-free asset—most commonly exemplified by the 10-year U.S. Treasury note—has regained its status as a formidable competitor for investor capital. For years, Bitcoin thrived in a low-interest-rate environment where the potential for explosive growth made the volatility of digital assets seem like a worthwhile trade-off. However, as central banks have maintained elevated interest rates to combat inflationary pressures, the math behind portfolio allocation has shifted dramatically. Investors are now presented with a clear choice: they can lock in reliable, guaranteed yields from government debt or expose themselves to the unpredictable price swings of the cryptocurrency market without the guarantee of outsized returns.

This dynamic introduces the concept of opportunity cost in its most acute form. When Bitcoin’s Sharpe Ratio—a measure of risk-adjusted performance—slides toward multi-year lows, it signals that the compensation for enduring market turbulence is no longer sufficient. Every dollar held in a volatile asset like Bitcoin is a dollar not earning the “risk-free” rate currently offered by bonds. When the so-called “crypto premium” fails to materialize, capital naturally begins to rotate out of speculative assets and into the relative safety of fixed-income securities. The cost of holding Bitcoin is no longer just the potential for a price drop; it is the tangible loss of the interest income that could have been earned elsewhere with virtually zero risk of default.

The psychological impact of this shift is profound for both retail and institutional participants. For retail investors, the allure of “moonshot” returns often blinds them to the necessity of risk-adjusted thinking, yet even the most hardened crypto enthusiasts become uneasy when the broader financial market offers a stable, high-yield alternative. Meanwhile, institutional investors are bound by fiduciary duties that prioritize capital preservation. When the Sharpe Ratio dips, these large-scale players face internal pressure to rebalance their portfolios, shedding riskier assets in favor of instruments that provide predictable cash flows. This exodus is not necessarily a rejection of Bitcoin’s long-term utility, but rather a cold, calculated response to the reality that in an era of high interest rates, cash is finally earning its keep.

The waning Sharpe Ratio serves as a market barometer: when the risk of volatility outweighs the reward of growth, capital flows will invariably gravitate toward the certainty of sovereign yields.

Ultimately, this trend highlights a maturing market that is increasingly sensitive to global monetary policy. As long as bonds offer competitive yields, Bitcoin must justify its existence through superior performance that exceeds the benchmark set by the traditional financial system. If the digital asset continues to struggle to provide that extra margin of return, the flight to safety will likely persist, forcing Bitcoin to either find a new catalyst for value appreciation or remain a secondary consideration in a yield-hungry investment climate.

Bitcoin does not exist in a vacuum; it is fundamentally tethered to the global financial ecosystem, where its performance is increasingly dictated by the shifting tides of macroeconomic policy. The recent decline in Bitcoin’s Sharpe ratio—a metric that measures risk-adjusted returns—serves as a clear signal that the asset’s historical ability to generate outsized gains relative to its volatility is currently under strain. This shift is inextricably linked to the Federal Reserve’s ongoing struggle with interest rate decisions and the broader contraction of global liquidity. When the cost of capital remains elevated, the speculative fervor that once defined Bitcoin’s bull runs tends to dissipate, forcing investors to re-evaluate the asset not just as a high-growth tech play, but as a component of a high-stakes portfolio that must now justify its volatility against the backdrop of more stable, yield-bearing alternatives.

The cooling of inflation and the subsequent recalibration of interest rate expectations have fundamentally altered the attractiveness of risk-on assets. For years, Bitcoin thrived in an environment of “easy money,” where low interest rates encouraged capital to flow into speculative ventures. However, as central banks prioritize restrictive monetary policies to temper inflation, the liquidity that once fueled Bitcoin’s parabolic moves has tightened significantly. This transition creates a new reality where the risk-reward profile is no longer skewed in favor of the investor. As traditional markets become more sensitive to Fed rhetoric, Bitcoin has found itself caught in the crosshairs, struggling to maintain its momentum as the “risk-free rate” on government bonds becomes a more competitive and safer destination for institutional capital.

The Sharpe ratio acts as a barometer for market efficiency; when it slides, it indicates that investors are being forced to accept higher levels of volatility for diminishing returns, effectively signaling a period of market malaise.

Furthermore, there is a tangible correlation between traditional market liquidity and Bitcoin’s inherent price instability. When global liquidity dries up, market participants often retreat into defensive postures, leading to lower trading volumes and increased susceptibility to sudden price swings. This volatility, when coupled with stagnant or declining price action, serves to depress the Sharpe ratio further, as the asset fails to compensate holders for the inherent risks of a decentralized, 24/7 market. Investors must now navigate a landscape where macroeconomic data points—such as unemployment reports or CPI readings—act as primary catalysts for volatility, often overriding Bitcoin’s internal cycles. Ultimately, the decline in this metric is a cautionary tale, reminding market participants that until global liquidity conditions stabilize or improve, the path of least resistance for Bitcoin may remain constrained by the overarching gravitational pull of the wider macroeconomic environment.

When the Sharpe ratio dips to levels not seen since the turbulence of 2022, it is easy for market participants to feel a sense of urgency. However, viewing this metric in isolation often leads to reactionary decision-making that can undermine long-term wealth accumulation. A declining Sharpe ratio essentially indicates that the risk-adjusted returns of an asset are compressing; investors are effectively taking on more volatility for less incremental reward. Rather than viewing this as a definitive exit signal, it is more constructive to interpret it as a shift in market regime. History suggests that such periods of inefficiency are often the precursor to significant volatility, which can be daunting, but they are also characteristic of the consolidation phases that historically precede major cyclical shifts.

For the long-term investor, the distinction between short-term noise and structural market cycles is paramount. Markets do not move in a straight line, and the frustration of stagnant or choppy price action often masks the underlying progress of network adoption and institutional integration. During these periods, maintaining a robust investment thesis is the only reliable compass. If your original reason for holding Bitcoin—whether it be as a hedge against currency debasement or a digital store of value—remains intact, then temporary fluctuations in risk-adjusted performance are merely background noise. Investors who focus exclusively on the Sharpe ratio may find themselves selling during periods of maximum apathy, precisely when the risk-to-reward profile is quietly resetting for the next major leg of growth.

To navigate this environment, disciplined risk management strategies become more valuable than ever. Dollar-cost averaging (DCA) remains the most effective antidote to the anxiety induced by poor short-term metrics. By automating purchases, investors remove the emotional burden of trying to time the bottom, ensuring they accumulate assets across a spectrum of price points regardless of the current Sharpe ratio. Furthermore, diversification across broader asset classes can help mitigate the impact of Bitcoin’s idiosyncratic volatility, ensuring that a temporary period of underperformance does not compromise one’s overall financial health. These strategies allow an investor to remain positioned in the market without the need to constantly monitor daily fluctuations.

Success in volatile markets is rarely the result of perfect timing; it is almost always the byproduct of consistent, long-term adherence to a well-defined risk management framework.

Ultimately, the current compression in risk-adjusted returns should serve as a reminder that patience is an active component of an investment strategy, not a passive one. Periods where metrics look unfavorable are often the times when the most significant foundational work is being done. By zooming out to view the broader multi-year cycle, investors can detach from the immediate pressure of the chart and focus on the trajectory of the asset over a five-to-ten-year horizon. Staying the course requires a clear understanding that while the Sharpe ratio fluctuates, the long-term potential of the digital asset space continues to evolve independently of short-term market sentiment.

You must be logged in to post a comment.