The Growing Visibility of Climate Risk in Real Estate

For decades, the real estate market treated natural disasters as unpredictable “acts of God”—random, unfortunate events that didn’t fundamentally alter the long-term value of a neighborhood. However, that perception is undergoing a profound and necessary shift as the frequency and severity of extreme weather events move from the realm of statistical outliers to a constant, looming reality. Whether it is the recurring threat of wildfires in the West, intensifying hurricane seasons along the coasts, or unprecedented flooding in inland regions, climate risk is no longer a distant, theoretical concern for future generations. It has solidified into a tangible, immediate factor that is actively reshaping how properties are evaluated, insured, and priced.

This transformation is driving a fundamental change in how both buyers and lenders perceive risk. We are moving away from an era of blissful ignorance toward a more data-driven future where geographic stability is as critical as square footage or school district ratings. As insurance premiums in high-risk zones skyrocket—or, in some cases, become entirely unavailable—the hidden costs of homeownership are becoming impossible to ignore. Buyers are beginning to realize that a home’s price tag is only the entry point; the true cost of ownership must now account for the potential of catastrophic damage and the rising expense of maintaining a residence in a vulnerable climate.

The market is finally beginning to internalize the reality that geographic stability is a primary asset class, and ignoring environmental hazards is a financial liability that can no longer be deferred.

Consequently, the narrative is shifting from “if” a disaster might happen to “how often” it is likely to occur over the life of a thirty-year mortgage. This new layer of due diligence is forcing potential homeowners to look beyond the aesthetic appeal of a property and interrogate the land itself. When evaluating a potential purchase, savvy buyers are increasingly turning to sophisticated mapping tools and climate risk assessments to understand their long-term exposure. By treating climate vulnerability as a quantifiable financial liability rather than a stroke of bad luck, the real estate market is slowly preparing to demand a different kind of transparency—one that may eventually necessitate a significant adjustment in how we negotiate the price of a home.

Why Home Buyers Often Ignore Disaster Vulnerability

When searching for a new home, the decision-making process is rarely a purely clinical exercise in data analysis. Instead, buyers often succumb to a pervasive psychological phenomenon known as optimism bias, which leads them to underestimate the likelihood of negative events occurring in their own lives. In the context of real estate, this means that even when presented with clear flood maps or wildfire risk assessments, individuals tend to believe that a catastrophic event is something that happens to other people, not to them. This cognitive shortcut allows buyers to focus on the immediate joy of a renovated kitchen or a manicured lawn, effectively filtering out the abstract, long-term threats posed by climate change.

This emotional attachment is further fortified by the persistent, outdated myth of the “100-year flood.” Many buyers operate under the false assumption that if a major disaster occurred recently, they are effectively “safe” for the next century. This mathematical misunderstanding provides a dangerous sense of security, allowing buyers to treat property risk as a finite, solved problem rather than a dynamic and worsening reality. Because the human brain is wired to prioritize immediate sensory experiences—like the charm of a coastal view or the tranquility of a riverside property—the invisible, statistical probability of future destruction is systematically discounted in the price negotiations.

The desire for homeownership is an inherently optimistic act, one that requires a buyer to bet on the future value and stability of a specific plot of land, often blinding them to the environmental volatility that might undermine that very investment.

Furthermore, the structure of the current real estate market incentivizes this oversight. Real estate listings prioritize curb appeal, school districts, and square footage, while environmental hazard disclosures are often buried in stacks of legal paperwork that buyers frequently skim over in their rush to close the deal. Because mortgage lenders and insurance companies have historically provided a safety net—sometimes artificially suppressing the true cost of risk—buyers have had little economic incentive to demand a “disaster discount.” Consequently, the market remains inefficient; it reflects a buyer’s willingness to pay for a dream home while failing to account for the true, escalating cost of the ground it stands upon.

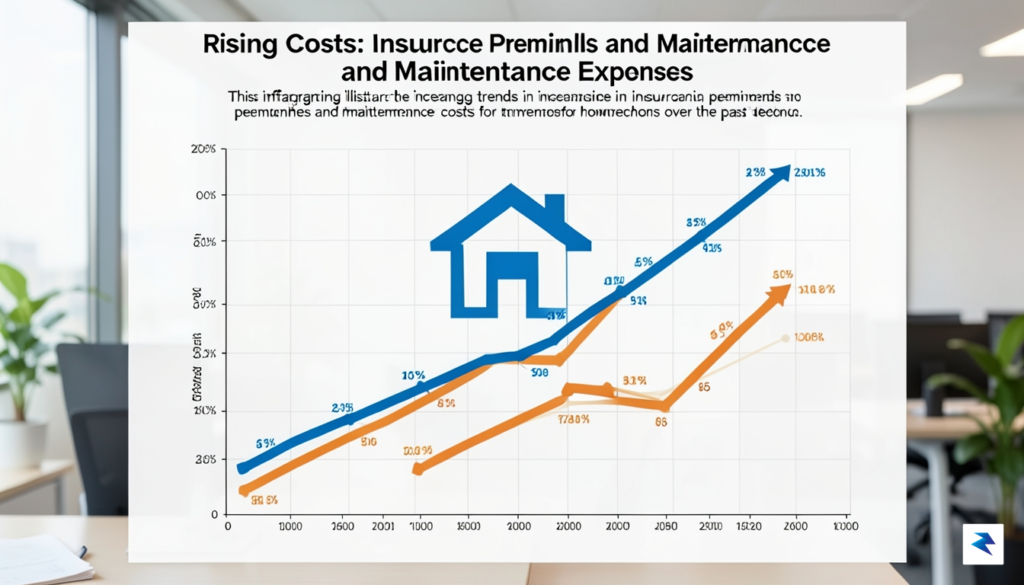

The Financial Reality: Insurance Costs and Market Value

When prospective buyers scout for a new home, they typically fixate on the mortgage payment, property taxes, and perhaps the local school district ratings. However, in regions increasingly vulnerable to climate-related catastrophes, a new, volatile variable is quietly eroding equity: the exploding cost of insurance. In states like California and Florida, the insurance market is undergoing a fundamental transformation that acts as a de facto tax on property ownership. As major insurers pull back or exit these markets entirely, homeowners are being forced into state-run “insurer of last resort” programs that offer significantly less coverage for exponentially higher premiums. This is not merely a budgetary inconvenience; it represents a structural shift in the long-term return on investment for residential real estate.

Consider the cumulative impact of these rising premiums as a hidden erosion of a home’s market value. If a buyer anticipates a monthly mortgage payment of $3,000, but is suddenly blindsided by a $1,000 monthly insurance premium—up from a negligible $200 just a few years ago—their purchasing power is effectively gutted. Because insurance costs must be accounted for in the debt-to-income ratios used by lenders, these rising expenses restrict the pool of potential future buyers who can qualify for a mortgage on that specific property. Consequently, when a home becomes prohibitively expensive to insure, its resale value inevitably plateaus or declines, as the market begins to bake climate risk into the listing price.

The most alarming prospect for today’s buyer is the potential for a home to become effectively uninsurable or, at the very least, unaffordable to protect. An asset that cannot be insured is essentially a liability, particularly if it is tied to a traditional 30-year mortgage that mandates coverage. If a property reaches a point where the cost of premiums exceeds the value of the protection, or where private carriers refuse to write policies altogether, the property may become frozen on the market. Future buyers will be unable to secure financing, leaving current owners trapped with an asset that is difficult to sell and impossible to safeguard against disaster.

The true cost of a home in a high-risk zone is no longer confined to the purchase price; it is increasingly defined by the mounting, recurring expense of climate-adjusted insurance premiums.

Ultimately, the era of ignoring climate risk is coming to a close as the financial sector begins to adjust its risk models. Buyers who fail to perform rigorous due diligence on the insurability and projected premium increases for a specific address are taking a significant gamble. By treating climate vulnerability as a primary financial metric—much like a credit score or a down payment—buyers can better protect themselves from the hidden costs that threaten to turn dream homes into long-term financial burdens.

Are We Reaching a Tipping Point for Risk-Adjusted Pricing?

For decades, the real estate market has operated under the assumption that property values only move in one direction: upward. However, as extreme weather events move from “once-in-a-century” anomalies to recurring seasonal threats, a quiet shift is occurring in how we value shelter. We are slowly approaching a potential tipping point where the “climate risk discount”—a price reduction intended to offset the future costs of flood mitigation, fire hardening, and skyrocketing insurance premiums—may finally become a standard feature of residential transactions. While retail buyers have historically prioritized aesthetics and school districts over long-term environmental hazards, the rising tide of insurance insolvencies and mandatory disclosure laws is forcing a more pragmatic, data-driven approach to home valuation.

Institutional investors have already begun to lead this charge, utilizing sophisticated catastrophe modeling to divest from or recalibrate their portfolios in high-risk zones. By treating climate vulnerability as a quantifiable liability rather than a distant abstraction, these entities are essentially performing a stress test on the housing market that individual buyers are only just beginning to emulate. When large-scale capital starts to retreat from a particular geography, it creates a ripple effect that eventually reaches the retail level; lenders become more conservative, insurance becomes prohibitively expensive, and the local tax base begins to wobble. This top-down pressure acts as a signal to the broader market that the era of ignoring environmental reality is rapidly drawing to a close.

Despite these market signals, the inevitable correction is arguably being delayed by a complex web of government subsidies and public-backed insurance pools. By artificially keeping insurance premiums lower than the true actuarial risk, federal and state programs prevent the market from seeing the “true” price of living in a high-risk area. This distortion creates a moral hazard: it encourages development in areas that are objectively unsafe while shielding buyers from the financial reality of their location choice. Critics argue that these safety nets are necessary to prevent a sudden housing collapse, yet supporters of market transparency contend that this intervention only exacerbates the eventual shock. If the government were to step back, the resulting price correction would likely be swift and severe, forcing a long-overdue recalibration of where and how we build our communities.

The transition toward risk-adjusted pricing is not merely a financial evolution; it is a fundamental shift in how society accounts for the true cost of environmental instability.

As we move forward, the question is no longer whether climate risk will influence home prices, but how quickly the market will adjust. Buyers who demand transparency today—investigating flood maps, fire history, and long-term infrastructure plans—are essentially early adopters of a new valuation paradigm. As more individuals factor these risks into their purchase offers, the “climate discount” will shift from a niche consideration to a baseline requirement. Ultimately, the market is beginning to recognize that a home is not just a place to live; it is a financial asset that must be protected against the physical volatility of the twenty-first century.

Strategies for Informed Home Buying in Vulnerable Regions

Purchasing a home is arguably the most significant financial commitment an individual will make in their lifetime, yet many buyers still rely solely on a standard property inspection to gauge the long-term viability of their investment. In today’s shifting climate landscape, a traditional checklist—which focuses primarily on the integrity of the roof, plumbing, and electrical systems—is no longer sufficient to protect your equity. To perform true due diligence, you must look beyond the physical structure and investigate the environmental narrative of the land itself. This requires a proactive approach that integrates historical data with future climate projections to ensure that your dream home does not become an uninsurable liability down the road.

Before you even consider submitting an offer, your research should begin with publicly available data that paints a clearer picture of regional risk. Start by consulting FEMA’s National Flood Hazard Layer to determine if the property sits within a designated high-risk zone, but do not stop there; look for local municipal records that detail past flood events, as official maps often lag behind current environmental realities. Simultaneously, research the local wildfire history of the area by accessing state forestry department records or regional climate portals. These tools provide a baseline understanding of whether the property has historically been in the path of destruction, allowing you to weigh the frequency of these events against your own tolerance for risk.

True due diligence in the modern era requires viewing a property not just as a static structure, but as a dynamic participant in its local ecosystem.

Once you have gathered the data, the next critical step is to have candid conversations with those who understand the financial implications of these risks best: local insurance agents. Before you commit to a purchase, request a preliminary insurance quote for the specific address to identify any “red flags,” such as high premiums, coverage exclusions, or difficulty securing a policy altogether. This financial reality check often reveals more about the property’s long-term viability than any seller disclosure form ever could. Furthermore, use this opportunity to ask the current homeowners about specific mitigation measures they have implemented, such as:

- Flood-proofing: Have they installed sump pumps, backflow valves, or raised mechanical systems above the base flood elevation?

- Fire-resistant landscaping: Has the property undergone “defensible space” clearing, or does it feature fire-resistant vegetation and non-combustible building materials like metal roofing or stucco siding?

- Structural reinforcements: Have any retrofits been completed to improve the building’s wind resistance or seismic stability, particularly if the home is located in a hurricane or earthquake-prone corridor?

By systematically vetting these factors, you move from a position of passive consumption to one of informed negotiation. If the property shows signs of environmental vulnerability, do not hesitate to use that information to adjust your offer price to account for future mitigation costs or the burden of rising insurance premiums. Ultimately, the goal of this deep-dive research is to provide you with the transparency necessary to make a decision that aligns with your financial future and your peace of mind.