The Equity Risk Premium Is Gone: What It Means for Your Portfolio

The Equity Risk Premium Paradox For decades, a fundamental pillar of investment strategy rested on the concept of the Equity Risk Premium…

When the United States and its allies first unveiled their comprehensive sanctions regime against Russia, a key objective was to significantly cripple the nation’s ability to export crude oil. The prevailing expectation was that these measures, including embargoes and price caps, would lead to a substantial reduction in Russian oil volumes reaching global markets, thereby severely impacting Moscow’s revenue streams and creating a notable supply crunch worldwide. Analysts widely predicted a dramatic reshaping of global energy flows, with a distinct and lasting reduction in Russian crude availability as Western buyers withdrew and logistical challenges mounted.

However, the reality that has unfolded in the months since has proven surprisingly different from these initial forecasts. Despite the unprecedented pressure, Russian crude export volumes have maintained a remarkable degree of stability. Recent detailed analysis indicates that the anticipated collapse in supply simply has not materialized as widely expected. Instead, data points to a consistent flow of Russian oil, suggesting a robust adaptation by the Russian energy sector and its trading partners that has defied the most severe predictions of economic isolation.

This persistent stability raises critical questions about the efficacy of the current economic measures in achieving their primary volumetric goals. The discrepancy between policy intentions and market reality underscores a complex interplay of global energy demand, geopolitical maneuvering, and the innovative workarounds developed to circumvent restrictions. It is not that sanctions have had no impact; rather, their effect has been felt more acutely in terms of pricing and logistical complexity, rather than an outright reduction in the quantity of crude leaving Russian ports.

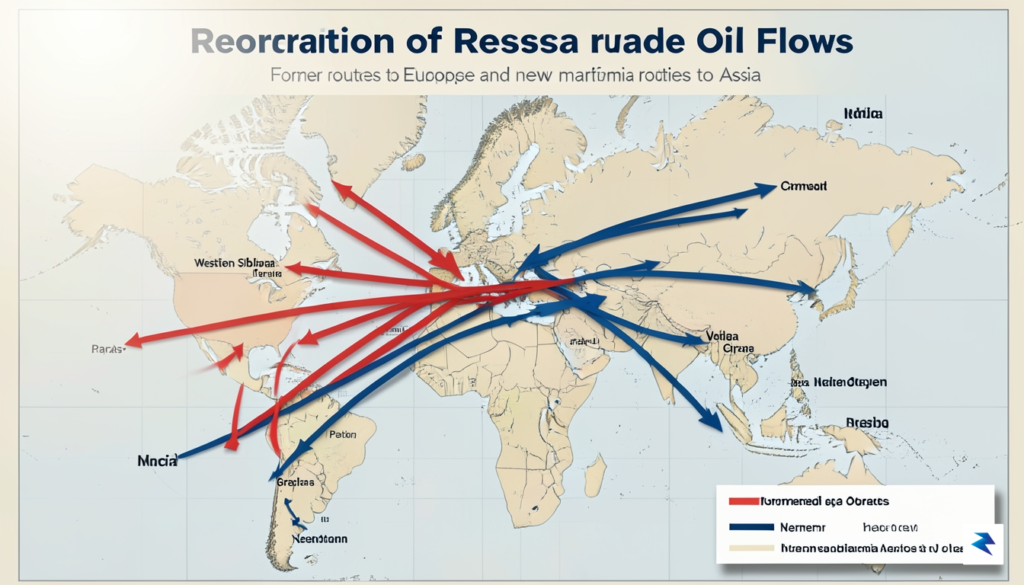

One of the most significant factors contributing to the resilience of Russian oil exports has been the rapid and effective reorientation of its export markets. Following the cessation of purchases by traditional European buyers, Russia swiftly pivoted its crude flows towards new, eager customers, predominantly in Asia. Nations like India and China, hungry for energy and less bound by Western sanctions, have stepped in to absorb the volumes previously destined for Europe. This strategic redirection has not only ensured a continuous outlet for Russian crude but has also fundamentally reshaped global oil trade routes, establishing new energy corridors that operate largely independently of Western influence.

Complementing the shift in buyers is the emergence and expansion of a sophisticated logistical network often referred to as the “shadow fleet.” This fleet comprises a growing number of tankers operating outside the conventional Western maritime insurance and shipping frameworks. These vessels, frequently older or re-flagged, are instrumental in transporting Russian crude to its new destinations, effectively circumventing restrictions on Western shipping services, insurance, and financing. This elaborate network of non-Western flagged ships, often operating with opaque ownership structures, has proven highly effective in maintaining the flow of oil, demonstrating a profound adaptability in global maritime logistics.

Furthermore, the mechanism of the price cap, while designed to limit Russia’s revenues, has also been navigated with strategic ingenuity. Russia has often found ways to sell its crude either just below the cap to buyers utilizing Western services or, crucially, entirely outside the G7-controlled shipping ecosystem when dealing with nations that do not rely on such services. The attractive discounts offered on Russian crude also act as a powerful incentive for non-Western buyers, ensuring a steady demand for these barrels regardless of the cap’s theoretical intent. This combination of market diversification, logistical innovation, and strategic pricing has allowed Russian crude export volumes to remain remarkably robust, fundamentally altering global energy trade patterns in the process.

The geopolitical landscape of global energy trade has undergone a profound and rapid transformation, fundamentally redrawing established supply lines. As traditional European buyers progressively scaled back or outright ceased imports of Russian crude oil following sanctions, Moscow swiftly reoriented its vast energy exports. This strategic pivot saw the flow of millions of barrels per day shift from westbound pipelines and Baltic Sea ports, predominantly serving European refineries, to eastbound maritime routes and newly prioritized Asian hubs. Nations like India and China, with their insatiable energy demands and willingness to engage, emerged as the primary beneficiaries and new linchpins of this reconfigured trade architecture, absorbing volumes that once fueled Western economies.

Executing such a massive reorientation required significant logistical ingenuity and infrastructure adjustments. While some crude could be redirected via existing pipelines to eastern destinations, the bulk of the shift necessitated an unprecedented expansion in seaborne transport. This involved not only an increase in tanker availability but also a complex rearrangement of shipping routes, extending voyage times considerably as tankers navigated thousands of additional miles around Africa to reach Asian ports. Furthermore, the development and optimization of port facilities on Russia’s Pacific coast, alongside robust ship-to-ship transfer operations in international waters, became crucial elements in maintaining the consistent flow of crude to its new markets.

A key catalyst in incentivizing this dramatic market reorientation was the strategic application of significant discount pricing for Russian crude. Faced with the immediate challenge of finding new buyers for its immense output, Russia offered its oil at notably lower prices compared to international benchmarks like Brent. This substantial discount proved irresistible for energy-hungry economies in Asia, particularly India and China, which were eager to secure reliable and more affordable supplies to fuel their industrial growth and burgeoning populations. The economic attractiveness of these discounted barrels effectively created a powerful pull factor, ensuring that Russian oil, despite Western sanctions, found ready and willing purchasers.

This rerouting of Russian oil is far more than a temporary workaround; it represents a deep-seated, structural shift in the global energy transit system with potentially long-lasting implications. The establishment of new, robust trade corridors between Russia and its Asian partners signifies a lasting recalibration of energy dependencies and geopolitical alignments. Traditional Western-dominated trade routes and financial mechanisms are now contending with a burgeoning parallel system, fostering a more multi-polar energy market. Ultimately, this reorientation underscores a fundamental reshaping of global energy security, where diversified supply chains and new bilateral relationships are emerging as defining characteristics of the next era of international energy trade.

The imposition of robust international sanctions against Russia’s energy sector sparked the rapid emergence of a sophisticated, parallel trade infrastructure designed to circumvent these restrictions. At the core of this adaptive response lies the proliferation of what is commonly referred to as the ‘shadow fleet’. This armada consists primarily of older tankers, often operating under flags of convenience from jurisdictions with less stringent oversight, and frequently changing their registered ownership to obscure their ultimate beneficiaries. These vessels act as the physical arteries of this clandestine trade, ensuring that Russian crude can still reach global markets by operating outside the traditional, regulated shipping ecosystem.

Circumventing the financial and insurance hurdles posed by sanctions has required equally inventive solutions. Western financial institutions and major insurance providers, particularly the dominant Protection and Indemnity (P&I) clubs, are largely unwilling or unable to service Russian oil shipments due to compliance risks. To bypass this, new financial channels have been established, often relying on non-Western banks in countries less aligned with the sanctions regime. Transactions frequently occur in non-dollar currencies, utilizing complex correspondent banking networks or even direct bilateral agreements, moving money through layers of intermediaries to obscure its origin and destination. Similarly, insurance coverage is secured through less transparent means, including self-insurance schemes backed by the Russian state, or smaller, often unregulated insurers operating out of various Asian or Middle Eastern hubs, thus providing a critical, albeit riskier, safety net for these voyages.

However, operating within these opaque trade routes introduces a host of significant risks. The aging nature of many shadow fleet vessels, coupled with potentially lax maintenance standards due to their unregulated status, raises serious environmental and safety concerns. There is an elevated risk of oil spills or maritime accidents, which could have devastating ecological and economic consequences, particularly in congested shipping lanes. Financially, the lack of transparency in transactions increases the potential for fraud, default, or disputes, as traditional legal and arbitration mechanisms are often inaccessible or ineffective in these grey areas. Furthermore, any legitimate entities that inadvertently interact with this shadow system face considerable reputational damage and the risk of secondary sanctions.

Regulators face an immense challenge in tracking and enforcing restrictions on this dynamic network. The sheer volume of global maritime traffic, combined with the deliberate tactics employed by the shadow fleet – such as switching Automatic Identification System (AIS) transponders off for extended periods, frequently changing flags, or engaging in ship-to-ship transfers in international waters – makes comprehensive monitoring incredibly difficult. While satellite imagery and advanced data analytics can provide insights, definitively identifying the ultimate beneficial owners of vessels or the precise financial flows remains a formidable task. This constant cat-and-mouse game between enforcement agencies and the adaptive mechanisms of the shadow fleet underscores the resilience and complexity of the workaround ecosystem that has emerged to sustain Russian crude exports.

The consistent flow of Russian crude into the global market, despite a comprehensive sanctions regime, presents a fascinating paradox that fundamentally influences global oil pricing. This persistent supply acts as a significant dampening force on what would otherwise be a far more volatile market. When a major producer like Russia continues to export at near-normal volumes, it cushions against potential supply shocks from other regions and helps to prevent sharp, speculative price spikes. Consequently, the stability observed in crude prices, even amidst ongoing geopolitical tensions, is partly attributable to the unexpected resilience of these Russian export channels, challenging initial expectations that sanctions would drastically curtail supply and drive prices skyward.

A key element in the policy toolkit, the G7 price cap, aimed to achieve a delicate balance: allow Russian oil to flow, thus preventing a global supply crunch, while simultaneously limiting Moscow’s revenue. However, the practical application of this cap has revealed its inherent limitations and the market’s ingenuity in circumvention. The emergence of a “shadow fleet” of tankers operating outside Western insurance and regulatory frameworks, coupled with a strategic pivot by Russia towards non-Western buyers in Asia, has allowed a substantial portion of its oil to trade above the cap. This adaptation underscores that while such measures introduce friction and additional costs, they have not proven to be an impenetrable barrier to trade, thereby reducing their intended impact on Russian earnings.

This reality forces a critical re-evaluation of whether current sanctions are achieving their intended strategic objectives of crippling Russia’s war economy and exerting significant geopolitical leverage. While the sanctions undeniably impose considerable transaction costs on Russia’s oil trade—manifesting as higher shipping, insurance, and financing expenses—they have not fundamentally halted the exports themselves. These increased costs are either absorbed by Russia through discounted prices or passed on to buyers, thereby making the trade less profitable but not impossible. The net effect is a less efficient, more complex global oil market, rather than one where a major producer is effectively shut out, suggesting that the primary impact has been on the mechanics of trade rather than its volume.

The implications extend broadly to global inflation and energy security. On one hand, the continued, albeit redirected, supply of Russian oil helps to mitigate upward pressure on global energy prices, thereby offering a subtle, indirect benefit in the ongoing fight against inflation worldwide. Preventing an acute supply shortage has likely spared consumers from even higher fuel costs. On the other hand, this reliance on an opaque, less regulated “grey market” for a significant portion of global oil trade introduces new vulnerabilities to energy security. It complicates monitoring, increases the risk of environmental incidents due to substandard shipping, and potentially strengthens geopolitical alignments that run counter to the objectives of sanctioning nations, fostering a more fragmented and less transparent energy landscape.

Ultimately, the resilience of Russia’s crude exports serves as a powerful testament to the global oil market’s remarkable liquidity and adaptive capacity. Policymakers initially envisioned sanctions as a potent economic weapon capable of swiftly altering geopolitical realities, but the market has demonstrated an unforeseen ability to re-route, re-price, and re-structure trade flows. This necessitates a sober reassessment of the effectiveness of economic sanctions as a tool for geopolitical leverage, particularly when applied to essential commodities. It suggests that while such measures can certainly increase friction and

The global energy landscape is undergoing a profound transformation, moving away from the integrated, interconnected system that defined the late 20th and early 21st centuries. We are entering an era of prolonged fragmentation, where nations increasingly prioritize energy security over the efficiencies of globalized trade norms. This shift manifests in a flurry of bilateral deals, the strengthening of regional energy blocs, and a pronounced desire to reduce reliance on single suppliers or vulnerable transit routes. Consequently, the traditional mechanisms for reconciling supply-demand imbalances, once largely dictated by global market forces, are now being tested by the complex interplay of geopolitical tensions, strategic alliances, and the persistent search for more resilient, localized energy configurations.

This strategic realignment introduces a fundamental tension between immediate energy security and long-term environmental objectives. While many nations remain committed to decarbonization goals, the urgent need to ensure stable and affordable energy supplies in a volatile world can, at times, push climate targets to a secondary concern. This often translates into renewed interest in domestic fossil fuel production or the securing of diverse conventional energy sources, even as investments in renewable energy technologies continue to grow. The result is a divergent global energy transition, where some regions accelerate green initiatives while others, facing immediate geopolitical pressures, lean on established energy frameworks, creating a complex and often contradictory path forward for global emissions reductions.

For investors and policymakers, navigating this evolving environment requires a sophisticated understanding of geopolitical risk and a flexible, adaptive strategy. Investors must recalibrate their risk assessments, diversifying portfolios across different energy types, geographies, and political systems to hedge against localized disruptions and policy shifts. Significant opportunities will arise in resilient infrastructure development, energy storage solutions, and innovative technologies that enhance energy independence or efficiency. Policymakers, on the other hand, face the monumental task of crafting robust energy diplomacy, fostering strategic international partnerships, and incentivizing domestic energy production and technological innovation to build more secure and sustainable energy futures for their populations.

Ultimately, the future of global energy markets will be characterized by a dynamic interplay of national interests, technological advancements, and evolving geopolitical realities. It will not be a simple return to past models, nor a smooth, linear progression towards a unified green economy. Instead, we can anticipate a mosaic of regional energy systems, diverse energy mixes, and a continuous negotiation between the imperatives of security, affordability, and sustainability. This complex, multi-polar energy world will demand persistent innovation, continuous adaptation, and a renewed focus on strategic resilience from all stakeholders.

You must be logged in to post a comment.