Bitcoin Reclaims $63,000: Analyzing the Mid-Year Market Reversal

Market Dynamics: Bitcoin’s Return to $63,000 The recent surge that propelled Bitcoin back above the $63,000 threshold represents a pivotal…

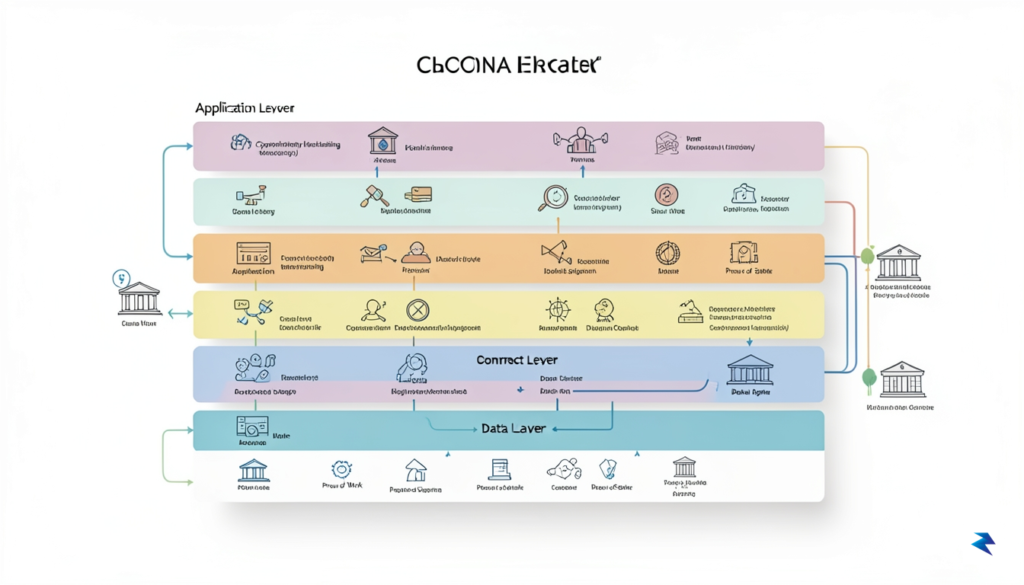

Tokenization, once a buzzword primarily associated with the fractional ownership of high-value assets like real estate or art, is rapidly maturing beyond its initial speculative phase. This revolutionary technology is no longer just about making illiquid assets accessible to a broader investor base; it’s evolving into a fundamental building block for an entirely new paradigm in multi-asset management. Industry leaders are now looking past simple asset fractionalization to unlock tokenization’s deeper potential, envisioning a future where it fundamentally reshapes how portfolios are constructed, managed, and optimized. This shift marks a pivotal moment, moving from theoretical promise to practical application in enhancing the sophistication and efficiency of wealth management.

Traditional financial systems, while robust, are inherently constrained by their legacy infrastructure. Portfolio construction in this environment often grapples with significant structural inefficiencies, particularly concerning liquidity and operational overhead. Managing a diverse portfolio of assets, from private equity to alternative investments, typically involves a labyrinth of manual processes, extensive paperwork, and fragmented settlement systems that can take days or even weeks to complete. This inherent friction not only drives up costs but also severely limits the agility and responsiveness required to implement dynamic investment strategies or achieve true, granular personalization for individual investors. The illiquidity of many alternative assets further exacerbates these challenges, creating barriers to entry and exit that restrict both diversification and strategic rebalancing.

Enter blockchain-based rails, which offer a transformative alternative to these outdated systems. Unlike traditional databases that merely store information, blockchain technology, through tokenization, introduces a programmable layer to financial assets. Here, a “token” is far more than just a digital representation of ownership; it’s a smart contract-enabled instrument embedded with rules, conditions, and functionalities that dictate its behavior. This programmability allows for automated execution of complex financial logic, such as compliance checks, dividend distributions, or even rebalancing triggers, directly at the asset level. Consequently, tokenization transitions from a mere storage mechanism to an active, intelligent participant in the financial ecosystem, paving the way for unprecedented levels of automation and customization.

By leveraging this programmable nature, tokenization directly addresses the structural inefficiencies plaguing traditional portfolio management. The inherent transparency and immutability of blockchain provide a single, auditable source of truth for all transactions, drastically reducing manual reconciliation and administrative burdens. Furthermore, by fractionalizing and digitally representing assets on a global, 24/7 infrastructure, tokenization dramatically enhances liquidity, making previously illiquid or hard-to-trade assets more accessible and tradable. This newfound liquidity, combined with the ability to automate complex investment strategies through smart contracts, empowers wealth managers to offer truly personalized portfolios that dynamically adapt to individual client needs, risk appetites, and evolving market conditions with unparalleled efficiency and speed.

The implications of this evolution extend far beyond simple cost savings or incremental improvements. We are witnessing the emergence of a new paradigm where portfolio construction is no longer a static, labor-intensive exercise but a dynamic, algorithmically driven process. This transformation unlocks the ability to create highly customized, multi-asset portfolios that can be managed with unprecedented precision and responsiveness, delivering on the long-sought promise of hyper-personalized wealth management. Ultimately, tokenization is not just digitizing existing assets; it is fundamentally redesigning the architecture of financial markets to be more efficient, accessible, and adaptable, paving the way for a truly innovative era in how wealth is managed and grown.

The traditional model of wealth management has long operated on a tiered structure, where bespoke portfolio construction and tax-optimized strategies were luxuries reserved almost exclusively for ultra-high-net-worth individuals. Today, the integration of blockchain technology is dismantling these barriers, ushering in an era of hyper-personalized portfolios that adapt in real-time to an investor’s unique risk profile, ethical preferences, and financial goals. By representing assets as digital tokens on a distributed ledger, financial institutions can now programmatically manage portfolios with a level of granularity that was previously hindered by manual overhead and high administrative costs.

At the heart of this transformation lies the power of smart contracts—self-executing code that resides on the blockchain. These digital protocols act as the automated engine for portfolio management, allowing for continuous, instantaneous rebalancing without the need for human intervention. When an investor’s risk appetite shifts or market volatility triggers a pre-defined threshold, smart contracts can automatically execute trades to bring the portfolio back into alignment with the user’s specific strategy. This mechanism ensures that tax-loss harvesting and asset allocation adjustments happen with surgical precision, effectively providing every retail investor with the kind of sophisticated, algorithmic oversight that was once the exclusive domain of institutional hedge funds.

The true promise of tokenization is not merely the digitizing of existing assets, but the creation of an infrastructure where complex financial strategies can be executed at scale, democratizing access to institutional-grade wealth management.

Furthermore, fractional ownership—made possible through the tokenization of real-world assets—is fundamentally reshaping the composition of individual portfolios. Investors are no longer restricted to broad-based index funds or a limited selection of stocks. Instead, they can now gain exposure to private equity, commercial real estate, hedge fund strategies, and bespoke derivatives in smaller, manageable portions. By breaking down high-barrier assets into smaller, liquid tokens, blockchain technology allows individuals to build highly diversified portfolios that were once geographically and financially inaccessible. This modular approach to asset ownership means that an investor can curate a portfolio that reflects their personal values or specific market outlook, blending traditional equities with private market opportunities in a single, seamless digital interface.

Ultimately, this shift toward hyper-personalization represents a move away from the “one-size-fits-all” investment products that have dominated the retail market for decades. As the friction of trading and the costs of administrative maintenance drop toward zero, the barrier to entry for complex, tailor-made investment strategies continues to evaporate. For the modern investor, this means that their financial future is no longer governed by the limitations of a rigid fund structure, but by a flexible, automated framework that evolves alongside their life circumstances and long-term financial objectives.

Transitioning from the theoretical potential of tokenized wealth management to a functional, enterprise-grade reality requires overcoming significant infrastructure bottlenecks. At the heart of this challenge is the fundamental need for seamless interoperability across disparate blockchain protocols. In an ideal ecosystem, a personalized portfolio might hold tokens representing assets that exist on different chains, ranging from private permissioned ledgers to public decentralized networks. Without standardized communication protocols, these assets remain siloed, preventing the fluid rebalancing and automated management that make tokenized portfolios so attractive to institutional investors. Developers are currently racing to build cross-chain bridges and interoperability layers that can maintain cryptographic security while allowing information and value to move frictionlessly across these technical boundaries.

Beyond the connectivity of networks, the industry must solve the complex puzzle of secure custody. Unlike traditional brokerage accounts where assets are held by a central intermediary, tokenized assets require digital wallets that are both highly secure and compliant with global financial regulations. Institutional-grade custody solutions must provide more than just private key management; they must integrate multi-party computation (MPC) and hardware security modules to ensure that funds remain protected against cyber threats while still being accessible for legitimate trading activity. As these portfolios become more granular and personalized, the custody infrastructure must be robust enough to handle high-frequency, automated movements without introducing systemic vulnerabilities or unnecessary latency.

Furthermore, the integrity of a personalized portfolio depends heavily on the accuracy of the underlying data. Because tokenized portfolios are intended to reflect real-world asset values, they rely on decentralized oracle networks to fetch and verify off-chain financial data. These oracles act as the essential bridge, feeding real-time price feeds, dividend schedules, and valuation updates into the smart contracts that govern the portfolio. If the oracle data is inaccurate or compromised, the entire automated engine could execute erroneous trades or misprice a client’s holdings. Consequently, the reliance on high-fidelity, tamper-proof data feeds is not merely an optional feature; it is a prerequisite for ensuring that the promise of personalized wealth management is built on a foundation of absolute technical precision.

The successful scaling of tokenized portfolios depends less on the blockchain itself and more on the invisible plumbing—the interoperability, secure custody, and verified data feeds—that connects decentralized technology to traditional financial requirements.

Ultimately, the goal is to create a seamless user experience that masks this underlying complexity. For the end investor, the technical implementation should be invisible, appearing as nothing more than an intuitive dashboard that reflects their unique financial goals. Achieving this level of simplicity requires developers to navigate a delicate balance: they must embrace the decentralized nature of blockchain technology while simultaneously layering on the rigorous compliance, identity verification, and auditability that financial institutions demand. As the infrastructure matures, the barrier to entry for tokenization will drop, paving the way for a new era of wealth management that is as agile as it is secure.

The integration of tokenized assets into the bedrock of traditional finance is less about a disruptive replacement of existing systems and more about a strategic evolution of how capital is managed, tracked, and deployed. For large asset managers, the path toward adoption requires a fundamental shift in operational philosophy, moving from legacy batch-processing models toward a real-time, programmable infrastructure. This transition necessitates that firms modernize their internal portfolio management systems (PMS) to support the unique metadata and security requirements inherent in blockchain-based assets. By creating a unified layer where traditional securities and tokenized private market instruments coexist, firms can achieve a level of operational efficiency that was previously impossible, effectively reducing the friction associated with settlement times and complex reconciliation processes.

Beyond the technical architecture, cultural transformation remains the most significant hurdle for established institutions. Leadership must foster an environment where legacy workflows are not seen as obsolete, but as the foundation upon which digital agility is built. This requires cross-departmental collaboration between compliance, IT, and investment strategy teams to ensure that tokenized assets adhere to rigorous regulatory frameworks while simultaneously leveraging the transparency of distributed ledgers. As firms begin to experiment with these new instruments, they must prioritize robust security protocols and interoperability standards, ensuring that their digital assets can move seamlessly across different environments without compromising investor safety or asset integrity.

True institutional adoption will be defined by the ability to augment existing wealth management frameworks with programmable layers, turning static portfolios into dynamic, responsive, and highly personalized investment engines.

Finally, the success of this transition hinges on a comprehensive commitment to education. Financial advisors serve as the primary bridge between complex financial innovation and the end-investor; therefore, they must be empowered with the knowledge to articulate the tangible benefits of tokenization—such as increased liquidity, fractional ownership, and automated compliance. When advisors are fluent in the nuances of digital assets, they can effectively demystify these instruments for clients, building the necessary trust to transition from traditional portfolios to more sophisticated, token-enabled structures. By demystifying the technology and focusing on the outcome—a more personalized and efficient investment experience—institutions can foster a long-term shift toward a future where digital and traditional assets operate as a single, cohesive ecosystem.

Navigating the regulatory landscape remains the most significant hurdle to the widespread adoption of personalized tokenized portfolios. While the promise of increased liquidity and fractional ownership is compelling, financial regulators globally are still grappling with how to classify and oversee digital assets that mimic traditional securities. Current frameworks, often designed for legacy clearing and settlement systems, are being stress-tested by the instantaneous nature of blockchain transactions. Consequently, institutional adoption is currently defined by a cautious “wait-and-see” approach, where compliance teams are meticulously mapping tokenized workflows against existing securities laws to ensure that investor protections, such as anti-money laundering (AML) and know-your-customer (KYC) requirements, remain robust in a decentralized environment.

Beyond the legal framework, the transition to a digital ecosystem introduces unique technical risks, primarily regarding smart contract vulnerabilities. In a tokenized world, the code is the contract; therefore, any flaw in the underlying programming can lead to irreversible loss or unauthorized transfers. Unlike traditional banking, where intermediaries can often reverse fraudulent transactions or correct administrative errors, blockchain-based assets operate on immutable ledgers. This creates a heightened need for rigorous auditing standards and formal verification processes for all smart contracts. Furthermore, counterparty risk takes on a new dimension in this space, as investors must not only trust the financial integrity of the issuer but also the security of the digital wallet infrastructure and the interoperability of the protocols hosting their personalized portfolios.

The evolution of digital finance is not a zero-sum game between innovation and regulation, but rather a necessary synthesis of both to ensure long-term market stability.

Looking toward the next five years, the industry is expected to pivot toward hybrid models that effectively bridge the gap between traditional compliance and blockchain-based agility. Major institutional players are unlikely to abandon the safety of centralized oversight; instead, they are likely to adopt permissioned blockchains that allow for transparency and speed while retaining the ability to enforce regulatory mandates. These hybrid platforms will likely feature “programmable compliance,” where regulatory checks are embedded directly into the token’s metadata. By combining the institutional trust of established firms with the automated efficiency of distributed ledger technology, the financial sector is poised to move past the experimental phase and into a new era where personalized, multi-asset wealth management becomes the standard for a broader range of investors.

You must be logged in to post a comment.