The AI Revolution: Inside the Factory Building Ukraine’s Next-Gen War Drones

The Evolution of Autonomous Warfare The landscape of global conflict is currently undergoing its most significant transformation since the…

For decades, the concept of generational wealth was often sequestered behind the heavy oak doors of traditional brokerage firms and complex financial institutions. Building a portfolio for a child previously required a significant amount of capital, a thorough understanding of jargon-heavy prospectuses, and the patience to navigate bureaucratic paperwork that felt more like a barrier than a gateway. Today, however, we are witnessing a tectonic shift in how families approach long-term financial security. The emergence of intuitive, mobile-first fintech platforms has democratized market access, transforming investing from an intimidating chore into a seamless, daily habit that fits comfortably within the rhythm of modern parenting.

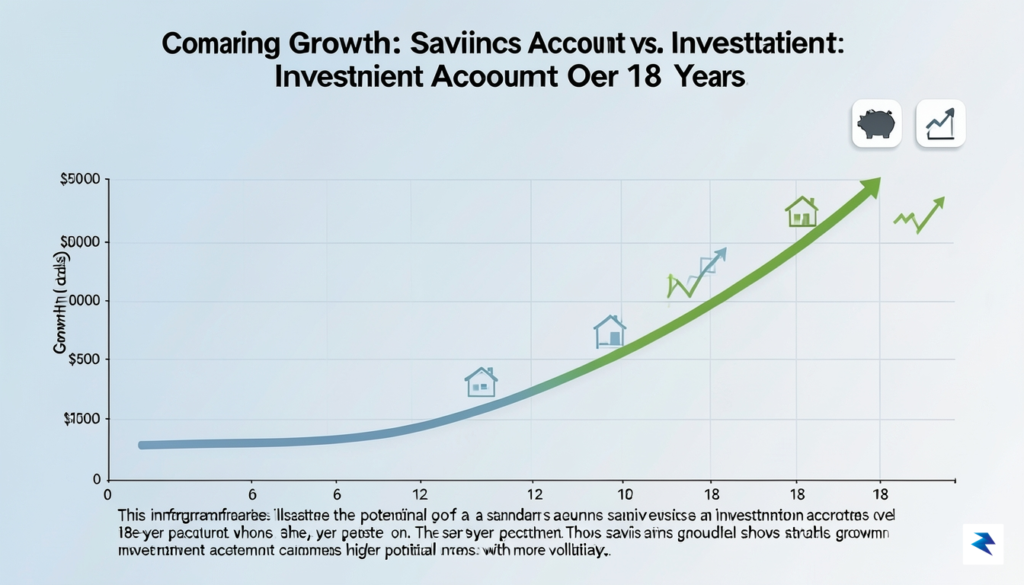

This evolution is defined by a move away from the stagnant security of traditional savings accounts, which often struggle to keep pace with inflation, toward the dynamic potential of market-based growth. Parents are increasingly recognizing that the real cost of “playing it safe” with a standard savings vehicle is the lost opportunity of compounding interest over an eighteen-year horizon. By utilizing modern applications that allow for micro-investments and automated contributions, families can now expose their children to the power of the stock market with as little as a few dollars a week. This accessibility does more than just grow a balance; it fundamentally changes the family’s relationship with money by turning passive saving into active wealth building.

Modern financial tools have effectively turned the intimidating process of wealth management into a transparent, visual experience that encourages long-term participation rather than short-term anxiety.

Beyond the technical ease of these platforms, there is a profound psychological benefit to this digital-first approach. When a child—and their parent—can open an app and witness the visual representation of their investments growing in real-time, it demystifies the stock market. Seeing a graph trend upward, even during periods of volatility, provides a tangible lesson in patience, discipline, and the efficacy of dollar-cost averaging. This immediate feedback loop fosters a sense of agency that was entirely absent in the era of passbook savings accounts. By prioritizing market exposure through these user-friendly interfaces, parents are doing more than just funding a college tuition or a first car; they are equipping the next generation with the financial literacy necessary to navigate a complex economy with confidence and clarity.

Ultimately, the transition toward these simplified financial ecosystems signifies a broader cultural acknowledgment: wealth building is no longer a luxury for the few, but a reachable goal for the many. As barriers continue to fall, the focus of family finance shifts from the difficulty of entry to the consistency of the journey. Whether it is through automated recurring deposits or gamified educational tools, modern fintech is ensuring that the concept of a “nest egg” is no longer just a metaphor, but a calculated, growth-oriented reality for every child.

Choosing the right financial vehicle for your child’s future is arguably the most crucial step in building a robust and successful long-term financial strategy. Beyond the simple savings account, a variety of sophisticated tools exist, each offering distinct advantages and considerations regarding taxes, control, and flexibility. Understanding these differences is paramount to ensuring your child’s assets grow efficiently and are available for their intended purpose, whether that’s higher education, a down payment on a home, or simply a

When it comes to building wealth for your children, time is not just a resource; it is the most potent financial instrument available to you. Unlike capital, which can be replenished through hard work or career advancement, time is a finite asset that, once spent, can never be recovered. By starting a dedicated investment account during your child’s infancy, you leverage the mathematical miracle of compound interest—the process where your earnings generate their own earnings. Even small, consistent contributions made during those early years can eclipse much larger sums invested later in life, simply because the money has more decades to snowball into a significant nest egg.

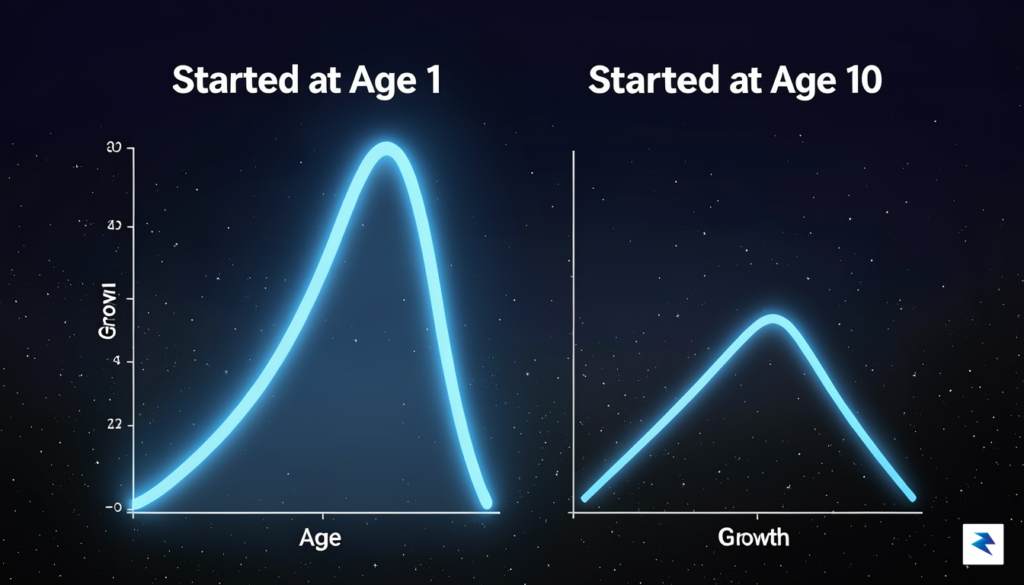

Consider the stark mathematical reality of starting early: if you invest $200 a month for a child starting at age 1, assuming an average annual return of 7%, your child could potentially reach adulthood with a substantial portfolio. Conversely, if you wait until your child is 10 years old to begin that same $200 monthly contribution, the total accumulation by age 18 will be drastically lower. That nine-year gap isn’t just a loss of time; it is a loss of the most aggressive growth phase of the investment. When you begin at age 1, the dividends and capital gains earned during the first decade are reinvested for the next seventeen years, creating a compounding effect that essentially does the “heavy lifting” for your child’s future financial independence.

The greatest gift you can give your child is not just the principal investment, but the gift of time, which allows the market to perform the heavy lifting on their behalf.

Beyond the raw math, adopting a strategy of dollar-cost averaging—investing a fixed amount at regular intervals regardless of market volatility—is essential for long-term success. By automating these contributions, you effectively remove the emotional bias that often leads investors to buy high out of excitement or sell low out of fear. When the market dips, your recurring contribution simply purchases more shares at a lower cost, positioning the portfolio for a stronger recovery. This disciplined, “set-it-and-forget-it” approach transforms investing from a stressful chore into a seamless habit. Over the span of eighteen years, this consistency creates a buffer against short-term economic fluctuations, ensuring that your child’s financial foundation is built on the steady, reliable growth of the broader market rather than the precarious timing of individual trades. Ultimately, by starting early and automating the process, you are teaching your child the most valuable lesson of all: that patience and consistency are the true architects of lasting prosperity.

While the prospect of building a financial nest egg for your child is undoubtedly rewarding, it is essential to approach custodial accounts—such as the Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) accounts—with a clear understanding of the underlying legal framework. When you open one of these accounts, you are essentially making an irrevocable gift to the minor. This means that the assets held within the account belong legally to the child from the moment they are deposited, even though you, as the custodian, maintain the authority to manage the investments until they reach the age of majority. Because these funds are legally the child’s property, they cannot be reclaimed or redirected for your own personal use, underscoring the importance of treating these accounts as dedicated vehicles for your child’s future rather than as flexible personal savings.

One of the most common concerns for parents is the potential tax burden associated with these investments, particularly regarding the so-called “kiddie tax.” Under current tax laws, a certain portion of a child’s unearned income—which includes interest, dividends, and capital gains generated within a custodial account—is exempt from federal income tax or taxed at the child’s lower rate. However, once that unearned income exceeds specific annual thresholds, the excess is taxed at the parents’ marginal tax rate. Navigating this requires careful planning; many parents choose to focus on growth-oriented assets that minimize annual taxable distributions or utilize tax-efficient investment strategies to stay within these thresholds, thereby preserving more capital for the child’s long-term benefit.

To maximize the growth of your child’s custodial account while staying tax-efficient, consider periodically reviewing your portfolio allocation to ensure that dividend-heavy investments do not inadvertently trigger higher tax liabilities that could eat into your long-term returns.

Perhaps the most significant milestone in the life of a custodial account is the transition of ownership, which occurs when the child reaches the age of majority, typically defined by state law as somewhere between 18 and 25 years old. At this specific point, the custodian’s legal authority terminates, and the child gains full, unfettered control over the account balance. This transition can be a nerve-wracking prospect for parents who worry about their child’s financial maturity. To mitigate this risk, it is vital to begin financial literacy conversations early, treating the account not just as a pot of money, but as a teaching tool. By involving your child in the decision-making process as they grow older, you can help ensure that when the legal transfer of control finally happens, they are well-prepared to manage those assets responsibly and continue the path of growth you started for them.

While establishing a dedicated savings account is a commendable first step toward your child’s financial independence, it serves merely as the foundation rather than the finished structure. The true value of these assets is realized only when your child understands the mechanics of how that money grows and the discipline required to maintain it. By involving your children in the investment process as they mature, you transform a passive financial vehicle into a dynamic classroom for real-world economic lessons. This transition from a simple “saver” mindset—which focuses on hoarding cash—to an “investor” mindset—which focuses on wealth accumulation and growth—is the most valuable inheritance you can provide.

One of the most intimidating yet essential concepts to master is the reality of market volatility. When the market experiences a downturn, it serves as a perfect, low-stakes teaching moment to explain that fluctuations are not synonymous with failure. Instead of shielding children from these realities, use them to demonstrate the value of long-term holding. By showing them how historical trends have generally trended upward despite periodic dips, you teach them to view volatility as a seasonal change in the weather rather than a permanent storm. This perspective fosters emotional resilience, preventing the impulsive decision-making that often ruins adult portfolios.

True financial literacy isn’t about knowing how to pick the next winning stock; it’s about understanding the power of patience and the compounding nature of time.

As your child transitions into their teenage years, you can move toward more collaborative decision-making. Start by involving them in small, low-risk portfolio reviews where you explain why specific assets were chosen for their long-term potential. You might consider allowing them to research a company they personally admire or interact with daily, using that as a springboard to discuss dividends, earnings reports, and the concept of ownership. This practical application bridges the gap between abstract numbers on a screen and the actual businesses that drive the global economy. By the time they reach adulthood, they will not just be the beneficiaries of a well-managed account; they will be the informed architects of their own financial future, equipped with the patience and knowledge to navigate the complexities of modern wealth management.

You must be logged in to post a comment.