The AI Jobs Crisis: What Economists Are Warning Policymakers About

The Economic Reality of the AI Transition The recent surge in artificial intelligence adoption has shifted rapidly from a fascinating…

The recent military exchanges between Iran and the United States have acted as an immediate catalyst for volatility, sending Brent and West Texas Intermediate (WTI) crude prices on a sharp upward trajectory. When geopolitical tensions flare in the Middle East, markets do not merely react to the physical destruction of infrastructure; they react to the specter of disrupted supply chains. Because a significant percentage of the world’s daily oil production transits through the Strait of Hormuz, any escalation in this theater forces energy traders to bake a “risk premium” into every barrel. This rapid price appreciation reflects a collective anxiety regarding the potential for broader regional instability to throttle the flow of energy to global industrial hubs, forcing investors to pivot toward safe-haven assets and energy-heavy portfolios in anticipation of further supply constraints.

Beyond the raw logistics of production and transport, the surge in oil prices is driven by a powerful psychological component that governs market sentiment during times of conflict. Financial markets operate on the anticipation of future scenarios, and the mere threat of a prolonged confrontation creates a feedback loop of fear and speculation. As headlines dominate the news cycle, algorithmic trading systems and human investors alike move to hedge against worst-case scenarios, effectively driving up the cost of futures contracts before a single drop of oil is actually lost to conflict. This behavior highlights a critical truth about the modern energy economy: the perception of scarcity is often just as potent as actual physical shortages when it comes to shifting global commodity pricing.

Historically, there is a well-documented correlation between Middle Eastern geopolitical instability and sudden spikes in crude oil pricing. Since the 1970s, conflicts in the Persian Gulf have repeatedly demonstrated that the global economy remains tethered to the stability of this specific region, regardless of advancements in renewable energy or domestic production in other territories. When tensions reach a fever pitch, the market reflexively looks back to previous crises—such as the Iran-Iraq War or the Gulf War—as a blueprint for what might occur next.

The volatility we are witnessing today is not just about the current strikes, but about the long-standing vulnerability of the global energy supply chain to regional politics.

By examining these historical patterns, it becomes clear that until a diplomatic cooling-off period is established, the market will likely remain in a state of hyper-vigilance. Investors are currently weighing the probability of a contained skirmish against the catastrophic risk of a total blockade, and as long as those two possibilities remain on the table, crude oil prices are expected to exhibit heightened sensitivity to even the smallest geopolitical tremors.

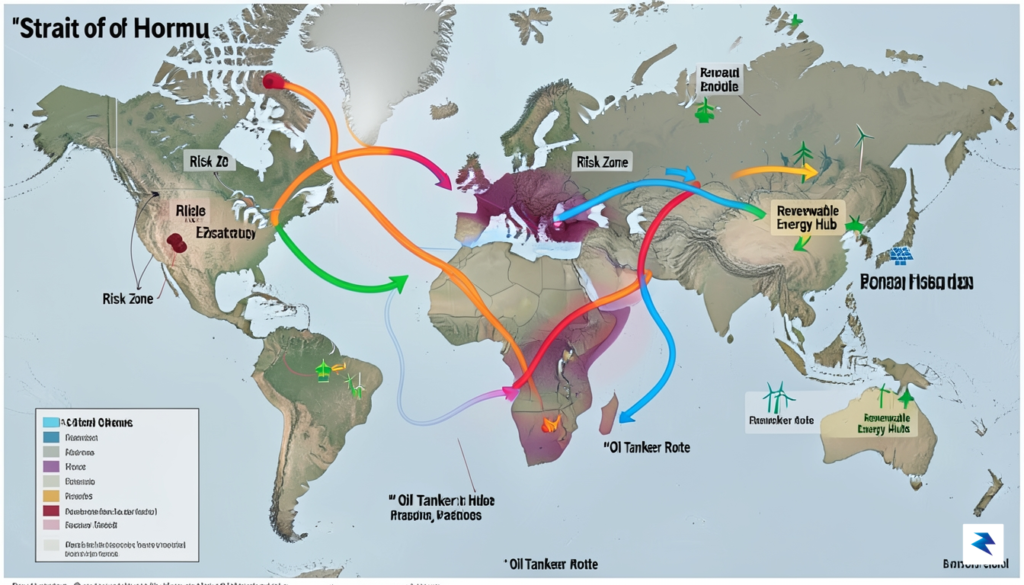

At the heart of the global energy landscape lies the Strait of Hormuz, a narrow maritime corridor that serves as the most critical chokepoint for international petroleum transit. Separating the Persian Gulf from the Gulf of Oman and the broader Arabian Sea, this waterway facilitates the movement of approximately 20 to 21 million barrels of oil every single day. This staggering volume accounts for roughly one-fifth of the world’s total petroleum consumption, making the Strait an indispensable artery for the global economy. Because so much of the world’s energy supply is funneled through this single point, any geopolitical friction in the region acts as an immediate catalyst for volatility, threatening to disrupt the delicate balance of supply and demand that keeps industrial nations running.

The geographical vulnerability of the Strait is perhaps its most defining feature, as it measures only 21 miles wide at its narrowest point. This constrained passage forces massive oil tankers to navigate through shipping lanes that are merely two miles wide for both inbound and outbound traffic, leaving them exceptionally exposed to regional hostilities or tactical blockades. Because these tankers are so restricted in their movement, they become easy targets for state-sponsored intimidation or accidental collision, heightening the risk of a catastrophic supply chain failure. This physical bottleneck means that even a minor disruption—whether it be a military standoff, a naval exercise, or a direct act of sabotage—can ripple outward, creating sudden, acute shortages that force markets to react with aggressive price hikes.

The strategic weight of the Strait of Hormuz is such that it functions as the ultimate barometer for global energy security; when the water is calm, the world economy breathes, but when tensions rise, the entire system enters a state of high-alert.

In response to these recurring regional threats, the global shipping industry has developed a highly sensitive mechanism for assessing risk: insurance premiums. When the political rhetoric between major powers intensifies, underwriters immediately classify the Strait as a “high-risk” zone, causing the cost of insuring both the vessels and their liquid cargo to skyrocket. These increased operational costs are not absorbed solely by the shipping companies; rather, they are passed down the line, eventually manifesting as higher retail prices at gas stations and increased energy costs for manufacturing sectors worldwide. Consequently, the Strait of Hormuz is not merely a geographic location, but a financial nerve center where political instability is converted, with frightening efficiency, into the rising cost of everyday life.

The recent escalation of hostilities between Iran and the United States has served as a stark reminder that global energy markets remain tethered to the fragile stability of geopolitical hotspots. While traders often react to the immediate shock of price fluctuations, the more profound consequence of these tensions is a systemic reassessment of what it truly means to have a resilient energy supply chain. For decades, the global economy operated under the assumption of relatively uninterrupted flow; however, the reality of localized conflict has forced nations to treat energy security not merely as an economic variable, but as a core pillar of national defense strategy.

As governments grapple with the vulnerability of relying on volatile trade routes, there is a palpable shift toward aggressive energy diversification. This transition is no longer just about environmental mandates; it has become a matter of sovereign survival. Nations are increasingly scrutinizing their dependence on single-source imports and are actively reconfiguring their energy portfolios to include a broader mix of domestic production, regional partnerships, and accelerated investment in alternative energy technologies. By reducing the weight of any single geopolitical actor in their energy balance sheet, countries aim to insulate their domestic industries from the cascading effects of distant military engagements.

True energy security is found not in the absence of conflict, but in the redundancy of supply.

To mitigate the immediate, gut-wrenching impacts of these supply shocks, strategic petroleum reserves continue to serve as the primary buffer. These massive stockpiles, held by major economies, act as a vital safety net, providing the necessary breathing room to manage market volatility while diplomatic channels work to de-escalate tensions. However, relying solely on these reserves is a temporary solution that cannot substitute for long-term structural changes. Policymakers are realizing that while reserves can dampen the spike in retail fuel prices, they do not resolve the underlying supply chain fragility exposed by the Strait of Hormuz tensions.

Ultimately, the future of global energy security will be defined by an era of strategic autonomy. This involves a dual-track approach: maintaining the necessary infrastructure for conventional energy stability while simultaneously fast-tracking the infrastructure required for a more localized, diversified power grid. As the world navigates these turbulent waters, the focus is shifting away from the pursuit of the lowest possible cost toward the pursuit of the highest possible reliability. In this new landscape, the ability to withstand a sudden supply constriction is rapidly becoming the most valuable asset a nation can possess.

The immediate reaction from OPEC+ following regional instability is rarely impulsive; rather, it is a calculated game of supply calibration. Historically, the alliance has maintained a delicate balance, aiming to keep prices high enough to satisfy member budgets while avoiding the demand destruction that comes with record-breaking costs. As tensions flare, the coalition faces a crossroads: they can either maintain their current production quotas to stabilize the market or leverage the supply gap to bolster government revenues. If the threat to global shipping lanes persists, OPEC+ may feel pressured to signal a readiness to increase production to prevent a runaway inflationary spiral, though their actual capacity to ramp up output remains a subject of intense skepticism among energy analysts.

Major importing nations, particularly powerhouses like China and India, find themselves in a precarious position as they navigate this supply-side volatility. These nations rely heavily on Middle Eastern crude to fuel their massive industrial sectors, making them particularly vulnerable to any disruption in the Strait of Hormuz. To mitigate these risks, both countries have been aggressively diversifying their energy portfolios, investing in strategic petroleum reserves and securing long-term supply contracts with alternative producers in Africa and the Americas. By building these buffers, they aim to insulate their domestic economies from the immediate, knee-jerk price spikes that follow geopolitical outbursts, effectively buying themselves time to adapt if a conflict turns into a long-term blockade.

“The stability of the global energy market now rests as much on diplomatic corridors as it does on oil rigs; when supply lines are threatened, the only immediate shock absorber is the strategic cooperation between major consumers and the producers who rely on their consistent demand.”

Ultimately, the trajectory of oil prices will depend heavily on the effectiveness of international diplomacy. Efforts to de-escalate tensions in critical shipping lanes are currently the primary focus for global powers, as a full-scale disruption would force a catastrophic rerouting of tankers that the current global infrastructure is ill-equipped to handle. While military posturing grabs the headlines, the quiet, back-channel negotiations aimed at ensuring the free flow of maritime traffic remain the most significant tool for preventing a temporary price surge from evolving into a structural shift in the energy economy. Whether these efforts succeed will dictate whether this current volatility remains a transient market correction or a harbinger of a more prolonged period of energy insecurity.

For businesses and investors, the current geopolitical climate necessitates a shift from passive observation to a proactive, risk-mitigation mindset. When evaluating the impact of regional instability on energy markets, stakeholders should prioritize monitoring the VIX (Volatility Index) alongside the futures curve for Brent and WTI crude. A widening spread between near-term contracts and long-term futures often signals an acute market fear regarding immediate supply disruption, whereas a flattening curve might suggest that the market is beginning to bake in a “new normal” for higher energy costs. By keeping a close eye on these technical metrics, investors can better distinguish between temporary price spikes driven by headline-chasing algorithms and fundamental shifts in the global supply-demand balance.

Beyond technical market data, supply chain managers must reassess their exposure to energy-linked overhead. The immediate ripple effects of rising oil prices are rarely confined to the pump; they permeate through logistics, plastic production, and manufacturing energy costs. Businesses should consider implementing tactical hedging strategies, such as locking in fuel surcharges or diversifying shipping routes to avoid reliance on volatile regions like the Strait of Hormuz. Furthermore, establishing redundant supplier networks—even if they carry a higher premium—can serve as a crucial insurance policy against sudden systemic shocks that threaten to paralyze lean, just-in-time inventory systems.

The key to navigating periods of extreme geopolitical tension is not necessarily predicting the next strike, but rather building an organizational structure that can withstand the resulting price volatility without sacrificing long-term operational health.

Looking ahead, stakeholders must weigh the potential for a return to price stabilization against the reality of a sustained high-cost environment. While diplomatic breakthroughs or increased production from non-OPEC nations could provide downward pressure on prices, the current instability suggests that risk premiums may remain elevated for the foreseeable future. Investors should avoid the trap of assuming a quick reversion to historical price averages. Instead, companies that stress-test their bottom lines against prolonged energy inflation will be the ones that emerge resilient. By maintaining a balance between cautious liquidity management and strategic operational flexibility, businesses can turn this period of uncertainty into a test of their overall structural integrity.

You must be logged in to post a comment.