Inside Hyundai’s Groundbreaking Pivot to Internal Stablecoin Transfers

The Shift Toward Corporate Blockchain Integration For decades, the global financial operations of massive industrial conglomerates have relied…

The sudden upward trajectory of crude oil prices in recent days serves as a stark reminder of the tenuous nature of global energy security. As hostilities intensify along critical maritime transit points, the immediate response from international markets has been one of heightened caution, pushing benchmarks higher as traders scramble to hedge against potential supply chain bottlenecks. This volatility is not merely a reaction to current shipments being delayed or diverted; rather, it reflects a deep-seated anxiety regarding the structural integrity of global trade routes. When conflict flares in regions that serve as the arteries of the oil industry, the ripple effects are felt instantly at the pump, proving that our modern energy landscape remains tethered to the physical safety of distant, localized corridors.

At the heart of this market agitation is the concept of a “risk premium,” a surcharge that investors and buyers willingly pay to account for the heightened possibility of physical disruption. When shipping lanes become hazardous, the cost of insurance for tankers skyrockets, and the time required to move energy from production hubs to demand centers increases as vessels are forced to take longer, safer, and more expensive routes. Consequently, the price of crude is no longer just a calculation of supply and demand fundamentals, such as extraction rates or seasonal consumption; it now includes a volatile layer of “geopolitical insurance” that fluctuates daily based on the latest headlines. This news-driven sentiment creates a feedback loop where even the anticipation of a blockade can trigger significant price swings, often independent of actual supply losses.

The integration of geopolitical risk into energy pricing acts as a permanent tax on global economic stability, forcing stakeholders to constantly recalibrate their expectations of what constitutes a ‘normal’ price for crude.

We are currently witnessing a fundamental redefinition of what “pre-war” price benchmarks mean for the global economy. For years, markets operated under the assumption that major shipping lanes would remain open and secure, allowing for relatively predictable pricing models. However, the current reality of persistent, localized instability has shattered this complacency, forcing analysts to adjust their long-term forecasts to account for a new, more dangerous paradigm. As these disruptions continue to influence futures pricing, both investors and consumers must contend with the fact that the era of easily accessible, low-risk energy transport is being replaced by a landscape where geopolitical friction is the primary driver of market uncertainty. This shift demands a more resilient approach to energy policy, as the fragility of our supply chains is no longer a theoretical risk, but a daily market reality.

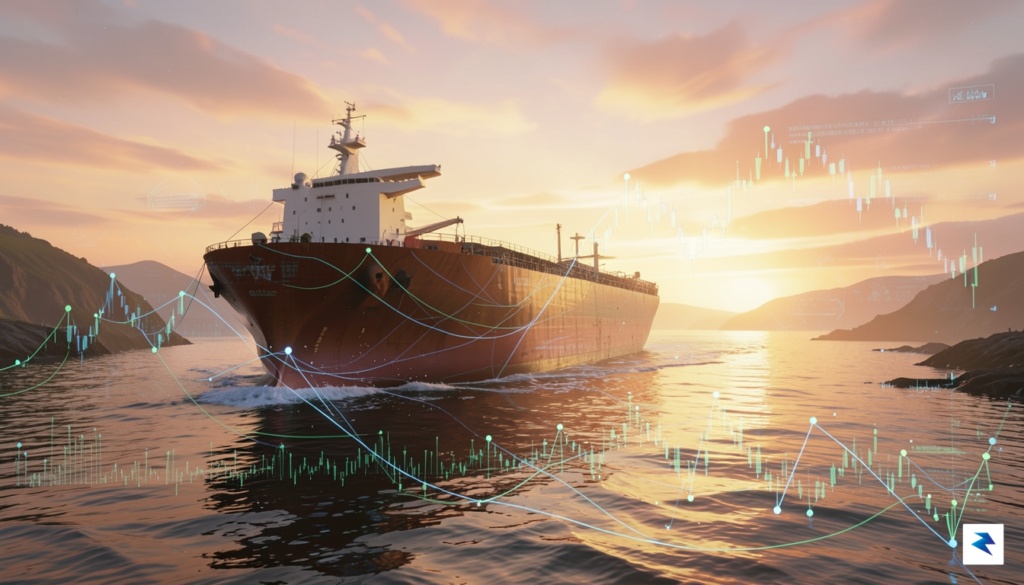

When commercial vessels, the lifeblood of global commerce, suddenly become targets in volatile regions, the meticulously planned logistics of international trade are thrown into immediate disarray. This isn’t merely a matter of isolated incidents; it triggers a systemic shift in how goods are moved across oceans, causing a rapid recalibration of routes and risk assessments by shipping companies worldwide. The impact is felt most acutely at critical maritime chokepoints, narrow passages through which a disproportionately large volume of global shipping must pass. Think of strategic arteries like the Suez Canal, the Strait of Hormuz, or the Bab el-Mandeb Strait; their disruption or perceived insecurity creates an instant bottleneck that can paralyze vast segments of the world’s supply chains.

The first and most direct consequence of heightened security concerns is a dramatic surge in operational costs, spearheaded by escalating insurance premiums. Shipping companies operating in areas designated as high-risk face significantly increased “war risk” surcharges from underwriters, which can add hundreds of thousands, or even millions, of dollars to the cost of a single voyage. This isn’t a minor administrative fee; it’s a substantial financial burden that directly impacts the profitability of transporting goods. Moreover, many insurance policies may even refuse coverage for certain high-risk zones, forcing vessels to either accept enormous uninsured risks or, more commonly, seek alternative, safer routes, further compounding the logistical challenges.

Consequently, the redirection of shipping lanes becomes an unavoidable reality. When major maritime passages are deemed too dangerous, ships are compelled to abandon their direct courses and embark on significantly longer detours. For instance, vessels avoiding a troubled chokepoint might opt for routes around entire continents, adding thousands of nautical miles to their journey. This is not a simple matter of choosing a different road; it translates directly into extended transit times, sometimes adding weeks to what would otherwise be a straightforward passage. Such delays create a cascading effect throughout the supply chain, pushing back delivery schedules, disrupting manufacturing processes reliant on just-in-time inventory, and causing widespread uncertainty for businesses and consumers alike.

The quantitative impact on transit times and operational costs for shipping companies is staggering. A longer journey means burning substantially more fuel, which is often the single largest operational expense for a vessel. Furthermore, extended voyages necessitate increased crew wages, additional provisions, and greater wear and tear on the ship itself, all contributing to a higher overall cost per trip. For a large container ship or oil tanker, rerouting around a continent can add anywhere from 10 to 20 days to a journey, consuming hundreds or even thousands of extra tons of fuel. These additional expenses are inevitably passed down the line, contributing to higher prices for everything from consumer goods to raw materials, including, most notably, crude oil.

Ultimately, these immediate supply chain disruptions are not merely inconveniences; they are costly logistical hurdles that reverberate profoundly through the global economy. The ripple effect extends far beyond the shipping industry, touching every sector that relies on timely and cost-effective maritime transport. When the arteries of global trade become congested or diverted due to security threats, the pulse of the world economy slows, demonstrating just how fragile and interconnected our global supply chains truly are in the face of geopolitical friction.

The recent surge in hostilities targeting commercial vessels has exposed the fragile architecture of the global energy supply chain, turning routine transit routes into zones of high-stakes uncertainty. When tanker operators are forced to reroute around dangerous maritime corridors, the immediate consequence is a dramatic increase in freight costs and voyage times. These logistical hurdles do not merely represent a temporary inconvenience; they act as a direct inflationary catalyst for crude oil. By extending the distance oil must travel to reach its destination, shipping companies face skyrocketing insurance premiums and fuel consumption costs, expenses that are inevitably baked into the final price of every barrel of crude delivered to refineries.

Beyond the logistical reality of longer voyages, the market is currently grappling with a climate of intense speculative trading. Financial markets often react to geopolitical instability with an “uncertainty premium,” where traders bid up the price of oil contracts in anticipation of future supply shortages. This speculative behavior feeds a feedback loop: as news of shipping delays circulates, traders purchase more futures, which drives up current spot prices even before a physical shortage has fully materialized. Consequently, the energy sector finds itself in a state of hyper-sensitivity, where the physical security of transport routes dictates market sentiment as much as the actual supply-demand balance of oil itself.

The intersection of maritime insecurity and energy pricing demonstrates that oil is not just a commodity, but a product of its own complex, fragile delivery infrastructure.

This tightening of shipping capacity creates a significant supply bottleneck that ripples through the entire petroleum lifecycle. When tankers are tied up on longer routes, there are fewer vessels available to move product globally, effectively shrinking the “virtual supply” of available oil. This scarcity forces refineries to pay a premium for consistent delivery, which compresses their refining margins. Ultimately, these increased operational costs are passed down the chain, manifesting as higher prices at the gas pump and increased utility costs for the end consumer. As long as shipping lanes remain compromised, the inflationary pressure on energy commodities will likely persist, illustrating that the global economy is only as stable as the maritime routes that sustain it.

For decades, the global economy operated under the assumption that the world’s maritime arteries—the narrow straits and canals that facilitate the flow of crude oil—would remain perpetually open. This reliance on “just-in-time” logistics transformed international trade into an efficient, albeit rigid, system where any deviation from the norm creates immediate, cascading pressure on prices. The current volatility serves as a stark reminder that our global infrastructure is far more fragile than once assumed. When geopolitical hostilities flare, the illusion of seamless connectivity shatters, revealing a structural over-reliance on singular, high-risk transit routes like the Red Sea or the Strait of Hormuz. These bottlenecks, which handle a staggering percentage of the world’s energy supplies, are no longer just strategic assets; they have become systemic liabilities that threaten the stability of global energy markets.

The hardening of the maritime risk market further illustrates this shift in perspective. Shipping insurers, once willing to offer predictable premiums for vessels traversing these hotspots, are now reassessing the very nature of maritime peril. As risks escalate, insurance rates for vessels operating in volatile zones have surged, forcing energy companies to either absorb these costs—thereby pushing up the final price of oil—or reroute their fleets entirely. This phenomenon of “re-routing” is not merely a logistical inconvenience; it is a fundamental shift in trade patterns that adds thousands of miles and weeks of transit time to critical supply lines. Consequently, the efficiency gains that once characterized global trade are being systematically eroded by the necessity of navigating around these new, man-made barriers.

The fragility of our current supply chain is not a temporary glitch; it is a permanent feature of a world where geopolitical friction can instantly turn a vital trade route into a high-risk zone.

Looking ahead, the energy sector is being forced to grapple with the urgent need for long-term diversification. Relying on a single maritime path is increasingly viewed as a failure of risk management rather than a standard operating procedure. Industries are beginning to explore alternative transport methods, including the expansion of pipeline infrastructure and the development of more resilient, multi-modal supply chains that do not depend solely on a handful of vulnerable waterways. While these investments require significant capital and time, the alternative—continued exposure to the unpredictable ebbs and flows of regional conflict—is becoming an unsustainable gamble. The transition toward a more diversified energy transport network will likely be a slow and arduous process, yet it is essential for decoupling global economic health from the volatility of localized geopolitical disputes.

As the global energy landscape faces increasing pressure from recurring geopolitical flashpoints, market participants are shifting their focus toward long-term stabilization strategies that transcend mere reactionary trading. The inherent fragility of maritime corridors, which currently serve as the lifeblood of global crude supply chains, necessitates a fundamental rethink of infrastructure resilience. For energy markets to thrive amidst this new era of instability, stakeholders must prioritize the diversification of transport routes and invest in redundant logistics networks. By reducing reliance on singular, vulnerable chokepoints, the global economy can better insulate itself from the sudden price spikes that follow localized conflict, effectively creating a more robust buffer against regional systemic shocks.

Strategic Petroleum Reserves (SPR) are also poised to take on a more prominent, proactive role in maintaining equilibrium. Rather than functioning solely as an emergency stopgap during extreme shortages, these stockpiles are increasingly viewed as a geopolitical tool designed to dampen the volatility caused by shipping disruptions. By strategically releasing reserves in response to supply chain bottlenecks, governments can effectively signal market stability to traders, thereby curbing speculative panic. This approach requires a delicate balance; however, as energy policies continue to evolve, the integration of these reserves with international coordination efforts will likely become a cornerstone of global energy security, ensuring that short-term hostilities do not translate into long-term inflationary damage.

The interplay between urgent energy demands and the transition to sustainable sources creates a unique paradox: while nations are racing toward decarbonization, the immediate reality of global infrastructure remains tethered to oil-based energy dependencies.

Looking ahead, the tension between aggressive energy transition policies and our current dependence on fossil fuels will continue to define market behavior. As countries push for greener alternatives, the short-term necessity of oil remains absolute, creating a volatile transitional phase where supply chain disruptions have outsized impacts on economic growth. Investors must account for this “bifurcated reality,” where long-term capital is increasingly directed toward renewables, yet short-term profitability remains inextricably linked to the stability of traditional hydrocarbon logistics. Navigating this environment will require a sophisticated understanding of how geopolitical friction influences both the immediate price of crude and the long-term investment horizon. Ultimately, those who can anticipate and hedge against these supply chain vulnerabilities will be the ones best positioned to weather the inevitable fluctuations of an interconnected—yet increasingly fractured—global energy market.

You must be logged in to post a comment.