Reed Jobs on Building Yosemite and the Future of Biotech

Beyond the Legacy: Reed Jobs and the Evolution of Yosemite While the name Jobs undoubtedly carries immense historical weight, evoking a…

Before the advent of the Unified Payments Interface (UPI), India’s digital payment landscape, while growing, faced significant fragmentation and friction points. Consumers often navigated a maze of different payment methods – from bank-specific net banking portals and various digital wallets to credit and debit cards, each with its own set of procedures and interfaces. While these options offered some convenience, they rarely provided a truly seamless, real-time experience across the entire ecosystem. The sheer dominance of cash transactions underscored the challenge: there was a pressing need for a universally accessible, instantaneous, and interoperable system that could bridge the gap between financial institutions and everyday users, ultimately aiming to bring millions into the formal digital economy.

The Unified Payments Interface emerged as the groundbreaking solution to this challenge, fundamentally reshaping how money moves within India and setting a new global standard for real-time payments. At its core, UPI is an instant payment system developed by the National Payments Corporation of India (NPCI), acting as an interoperable layer that facilitates peer-to-peer (P2P) and person-to-merchant (P2M) transactions directly between bank accounts. Crucially, it is built upon the robust foundation of the Immediate Payment Service (IMPS), which was already operational, leveraging IMPS’s 24/7 real-time interbank transfer capabilities. This strategic layering allowed UPI to inherit reliability and speed while adding an unprecedented layer of user-friendliness and broad accessibility.

One of UPI’s most significant architectural shifts lies in its pivot from traditional card-based ‘push’ payments to an innovative account-based ‘pull’ mechanism. Historically, card transactions or net banking often involved the payer “pushing” funds to a merchant or recipient, frequently requiring sensitive details or navigating multiple authentication steps. UPI, conversely, empowers users to initiate transactions directly from their bank accounts using a simple Virtual Payment Address (VPA) or by scanning a QR code, effectively “pulling” funds with consent. This paradigm shift dramatically simplifies the user experience, eliminating the need to share bank account numbers or IFSC codes for every transaction, thereby democratizing financial access and making instant payments as easy as sending a text message.

The rapid and widespread adoption of UPI can be largely attributed to its meticulously designed, API-driven architecture. By providing standardized Application Programming Interfaces (APIs), UPI enabled a vast ecosystem of banks, fintech companies, and third-party payment applications (TPAPs) to integrate seamlessly with the core payment network. This open and collaborative framework fostered immense innovation, allowing diverse payment apps like Google Pay, PhonePe, Paytm, and numerous bank-specific applications to offer UPI services, each with unique user interfaces and value-added features. This interoperable infrastructure not only accelerated the onboarding of millions of users and merchants but also established UPI as a powerful benchmark for real-time payment systems worldwide, demonstrating how a well-structured digital public good can propel an entire economy forward.

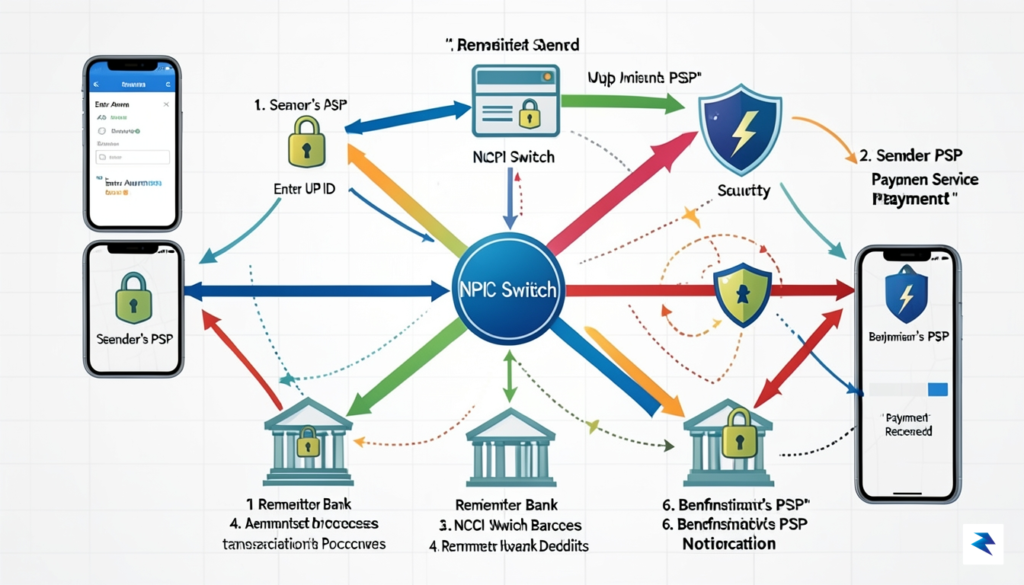

The seemingly simple act of tapping ‘Pay’ on your smartphone to complete a Unified Payments Interface (UPI) transaction initiates a complex, high-speed ballet of digital communication behind the scenes. In the blink of an eye, often within milliseconds, your payment request travels through a sophisticated network, engaging multiple entities before returning with a confirmation. Understanding this intricate journey reveals the engineering marvel that powers India’s real-time payment ecosystem.

The journey begins the moment you confirm the payment in your UPI-enabled application. Here, your app gathers critical information, primarily the unique Virtual Payment Address (VPA) of the beneficiary, the amount, and your own VPA. This VPA acts as a crucial abstraction layer, eliminating the need to share sensitive bank account numbers or IFSC codes, thus enhancing security and user convenience. Once you authorize the transaction, typically with your MPIN or biometrics, your Payment Service Provider (PSP) app – the financial institution that provides your UPI handle – springs into action, encrypting this data for secure transmission.

This encrypted payment request is then handed over to a crucial component: the National Payments Corporation of India (NPCI) Common Library. This standardized software development kit (SDK) or API is embedded within every UPI application and bank system, ensuring seamless and uniform communication across the diverse ecosystem of banks and third-party apps. The Common Library standardizes the transaction format and security protocols, acting as a universal translator that allows different banks and apps to speak the same technical language, preparing the request for its onward journey to the central NPCI switch.

Upon receiving the validated and encrypted request, the NPCI’s Central Payment Switch takes center stage. This highly robust and secure system acts as the central router and clearinghouse for all UPI transactions. It meticulously examines the sender’s VPA to identify the remitting bank (your bank) and the beneficiary’s VPA to identify their bank. In a fraction of a second, the switch routes an authorization request to your bank. Your remitting bank then verifies your identity, confirms the available balance in your account, and places a temporary hold on the transaction amount, ensuring funds are available before proceeding further.

With the remitter’s bank giving its nod, the NPCI Switch then forwards the payment instruction to the beneficiary’s bank. This instruction carries details about the transaction, prompting the beneficiary bank to credit the specified amount to the designated VPA, which maps to their customer’s bank account. Both the debit from the sender’s account (or rather, the release of the held amount) and the credit to the beneficiary’s account are designed to happen nearly simultaneously, maintaining the real-time nature of UPI.

The final leg of this journey involves a critical callback mechanism. Once both banks have successfully processed their respective parts of the transaction (debiting the sender and crediting the beneficiary), they send acknowledgments back to the NPCI Switch. The Switch, having received confirmation from both ends, then dispatches a final transaction status update to both the sender’s and beneficiary’s PSPs. These PSPs, in turn, update their respective apps, providing you with the instantaneous ‘Payment Successful’ or ‘Transaction Failed’ notification. This entire multi-party, multi-stage process, from the initial tap to the final confirmation, is executed with remarkable speed and precision, showcasing the architectural brilliance underpinning India’s digital payment revolution.

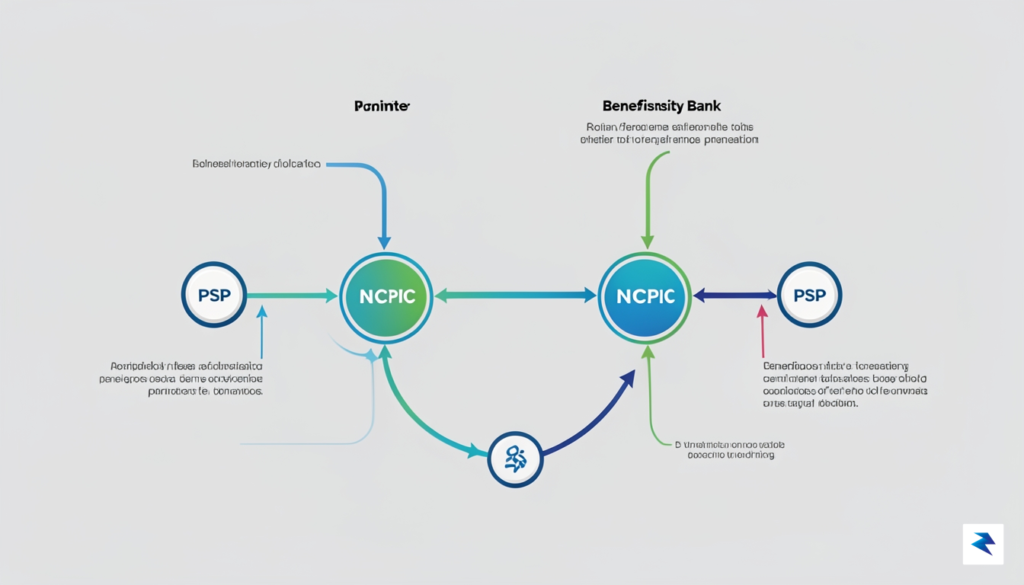

The remarkable efficiency and widespread adoption of India’s Unified Payments Interface (UPI) stem from its intelligently designed, decentralized yet intricately interconnected architecture. Rather than a single monolithic entity dictating the entire transaction flow, UPI operates through a collaborative ecosystem where distinct stakeholders play specific, vital roles. This distributed responsibility ensures resilience, scalability, and robust security, ultimately empowering millions of transactions daily without a hitch. Understanding these individual contributions is key to appreciating the underlying mechanics of this groundbreaking payment network.

At the forefront of the UPI experience are the Payment Service Providers (PSPs), which are essentially the customer-facing applications that users interact with daily. Think of popular platforms like Google Pay, PhonePe, Paytm, or your bank’s own UPI-enabled app. These PSPs are responsible for creating intuitive interfaces, managing user registration, linking bank accounts, and facilitating the initiation of payment requests. Their role extends beyond merely presenting a user interface; they also handle crucial aspects like generating Virtual Payment Addresses (VPAs), managing mandates, ensuring robust authentication mechanisms (like UPI PINs), and providing transaction history. PSPs act as the primary interface, translating complex banking processes into a simple, seamless user journey.

Bridging the gap between various PSPs and the underlying banking infrastructure is the National Payments Corporation of India (NPCI). Established as a not-for-profit organization, NPCI serves as the central switch and clearinghouse for all UPI transactions. When a user initiates a payment via a PSP, the request is routed through NPCI. Its core function involves authenticating the transaction details, validating the VPAs of both sender and receiver, and intelligently routing the payment request to the respective remitting and beneficiary banks. NPCI effectively acts as the orchestrator, ensuring that messages are correctly interpreted and relayed across the network in real-time. Furthermore, it plays a critical role in reconciliation, dispute resolution, and establishing the standardized protocols that all participants must adhere to, guaranteeing interoperability across the entire ecosystem.

Underpinning the entire UPI network are the traditional banking institutions. While PSPs provide the interface and NPCI handles the switching, it is the banks that hold the actual funds and execute the debits and credits. Every UPI transaction involves at least two banks: the remitter’s bank (where the sender holds their account) and the beneficiary’s bank (where the receiver’s account is held). Once NPCI authenticates and routes a transaction, these banks are responsible for validating the account balances, applying the necessary debits and credits, and ensuring that the funds are transferred securely. This process involves strict adherence to regulatory compliance, including Know Your Customer (KYC) and Anti-Money Laundering (AML) norms. Ultimately, banks are the custodians of the money, fulfilling the final leg of the transaction by moving the actual monetary value between accounts based on the instructions received through the UPI framework.

Security forms the bedrock upon which any successful digital payment ecosystem is built, and India’s unified payment interface (UPI) stands as a testament to this principle. Far from being a mere convenience, the system is engineered with a multi-layered security architecture designed to safeguard every transaction and protect users’ financial data with utmost vigilance. This comprehensive approach ensures that even as billions of transactions flow through the network, each individual payment remains private, secure, and impervious to tampering, fostering immense trust among its vast user base.

One of the foundational security measures is device binding, a crucial process that links a user’s unique bank account to their specific mobile device and registered phone number. During the initial setup, the UPI application verifies the user’s identity by sending an SMS from the registered mobile number associated with their bank account. This effectively creates a secure digital handshake between the user’s banking identity and their physical device, preventing unauthorized access or transaction initiation from any other handset. This robust mechanism ensures that even if someone manages to obtain your account details, they cannot initiate payments without access to your designated, bound device.

Complementing device binding is the indispensable role of multi-factor authentication, primarily through the use of the Mobile Personal Identification Number (MPIN). This four-to-six digit code acts as the second, critical layer of verification for every single transaction initiated on the platform. Much like a debit card PIN, the MPIN is known only to the user and is never stored in plain text by UPI or the participating banks, making it incredibly difficult for fraudsters to compromise. By requiring both the bound device and the correct MPIN for authorization, UPI significantly elevates the security posture of each payment, ensuring that only the legitimate account holder can approve financial movements.

Furthermore, all communication within the UPI network is shielded by sophisticated cryptographic standards through end-to-end encryption. From the moment a user initiates a transaction on their device until it reaches the recipient’s bank, every message and data packet is encrypted, transforming it into an unreadable code for anyone without the correct decryption key. This robust encryption protocol guarantees the privacy and integrity of transaction details as they traverse the vast digital network, effectively preventing eavesdropping, data interception, or any form of alteration during transit. It’s a continuous digital fortress ensuring data remains confidential and tamper-proof at every stage of its journey.

Even with these advanced preventative measures, the system also anticipates and addresses potential issues through a well-defined dispute resolution process. In the event of a failed transaction, an unauthorized debit, or suspected fraudulent activity, users have clear avenues to report and resolve these issues directly through their UPI app or bank. Banks and the National Payments Corporation of India (NPCI), the operator of UPI, work collaboratively to investigate such claims, often leveraging real-time transaction monitoring and advanced AI-driven fraud detection systems that continuously scan for unusual patterns. This proactive and reactive framework ensures that users have recourse and that the integrity of the financial ecosystem is maintained, reinforcing confidence in the platform’s ability to handle exceptions securely and efficiently.

While many nations have grappled with the complex task of building a real-time, low-cost, and highly scalable digital payment system, India’s Unified Payments Interface (UPI) stands out as a resounding success story. Its architectural brilliance lies in a deliberate prioritization of interoperability and a low-friction user experience, addressing critical pain points that often hinder the adoption of digital payments elsewhere. By analyzing its core design choices, such as the innovative Virtual Payment Address (VPA) system, we can uncover why UPI has become a global benchmark for payment innovation, far surpassing the capabilities of many legacy infrastructures.

One of the fundamental differences lies in UPI’s transaction model, which largely operates on a ‘push’ basis, rather than the ‘pull’ system prevalent in legacy card networks. In a traditional card transaction, the merchant ‘pulls’ funds from the customer’s account via the card network, requiring the customer to share sensitive card details. UPI, conversely, empowers the user to ‘push’ money directly from their bank account to the recipient’s VPA, typically requiring only a PIN for authorization. This push-based model significantly enhances security by minimizing the sharing of sensitive financial information and granting users explicit control over every transaction, reducing instances of fraud and chargebacks common in pull-based systems.

Crucial to UPI’s widespread adoption is its inherent interoperability, a feature often lacking in older payment infrastructures. The Virtual Payment Address (VPA) system is a cornerstone of this design, acting as a unique identifier for an individual’s bank account across the entire UPI network. Instead of needing to know complex bank account numbers and IFSC codes, users can simply send or request money using a memorable VPA, such as `name@bank`. This abstraction allows users to transact seamlessly between accounts held at different banks, using any UPI-enabled application, thus fostering intense competition among payment service providers and eliminating the fragmentation seen in systems where different banks operate in isolation.

Beyond convenience, UPI’s architectural design delivers unparalleled cost-efficiency, a stark contrast to the multi-layered fee structures that burden traditional payment rails. Legacy card networks involve multiple intermediaries—issuing banks, acquiring banks, card schemes (like Visa or Mastercard), and payment processors—each levying their own fees, culminating in significant Merchant Discount Rate (MDR) charges for businesses. UPI, by design, bypasses many of these layers, facilitating direct bank-to-bank transfers through a lean, centralized infrastructure. This drastically reduces per-transaction costs, enabling a near zero-MDR environment for many transactions in India and making digital payments accessible and affordable even for small street vendors.

The ease with which merchants can integrate UPI into their operations further cements its advantage over legacy systems. Unlike traditional point-of-sale (POS) systems that often require expensive hardware terminals, monthly subscriptions, and complex setup processes, UPI leverages ubiquitous smartphone technology. Merchants can simply display a static or dynamic QR code, which customers scan using their UPI app to initiate payment. This low barrier to entry has democratized digital payments, allowing even the smallest businesses to accept cashless transactions without significant upfront investment or recurring costs, thereby accelerating financial inclusion across diverse economic strata.

India’s Unified Payments Interface (UPI) has rapidly transformed the domestic digital payment landscape, establishing itself as a robust, real-time platform. Now, the innovative system is poised for an ambitious leap onto the global stage, with international partnerships expanding its reach far beyond national borders. This strategic expansion is set to position UPI as a significant global player, particularly in the realm of cross-border remittances, offering a faster, more cost-effective alternative to traditional channels. The vision is to enable seamless, instant payments between individuals and businesses across continents, mirroring the efficiency it has achieved domestically.

However, scaling such a sophisticated system for international interoperability introduces a complex array of technical challenges. One of the primary hurdles lies in managing multi-currency clearing and settlement. Unlike a single-currency domestic system, global transactions involve fluctuating exchange rates, varying settlement cycles, and the need for robust foreign exchange mechanisms. Building the underlying infrastructure to handle these complexities while maintaining the real-time nature of UPI transactions requires significant innovation in backend systems, including advanced reconciliation engines and sophisticated liquidity management frameworks capable of operating across diverse financial ecosystems.

Beyond the technical intricacies, navigating the patchwork of global financial regulations presents another formidable challenge. Each nation possesses its own unique set of rules concerning anti-money laundering (AML), know-your-customer (KYC) compliance, data privacy, and payment system oversight. Clearing these regulatory hurdles necessitates bilateral agreements, mutual recognition frameworks, and potentially the harmonization of certain standards to allow the UPI stack to function effectively and legally in different jurisdictions. Significant diplomatic and collaborative efforts are underway to forge these pathways, ensuring that the convenience of UPI does not compromise essential financial security and regulatory integrity.

The true potential of a globally integrated UPI lies in its ability to connect with other sovereign digital payment systems. Imagine a world where India’s UPI users can instantly send money to someone using Singapore’s PayNow, Thailand’s PromptPay, or the UAE’s Aani, and vice versa. Such integrations would create a vast, interconnected network of real-time payment rails, significantly reducing transaction costs and times for international transfers. These cross-system collaborations are not merely about convenience; they represent a fundamental shift towards more inclusive and efficient global financial architecture, fostering deeper economic ties and facilitating easier movement of funds for trade, tourism, and personal remittances.

Furthermore, the domestic success of “credit-on-UPI” capabilities offers a glimpse into how financial inclusion could expand globally. By linking pre-approved credit lines directly to the UPI interface, users can access small loans or overdraft facilities seamlessly for their daily transactions. Exporting this model to developing economies, particularly those with nascent credit markets, could unlock unprecedented access to formal credit for millions. It could empower individuals and small businesses with instant liquidity, fostering economic growth and reducing reliance on informal, often predatory, lending practices, thereby extending the transformative impact of UPI beyond just payments to broader financial empowerment.

Ultimately, UPI’s journey from a domestic marvel to a global force is a testament to its foundational strength and adaptability. While the path is fraught with technical and regulatory complexities, the ongoing expansion, the strategic alliances, and the continuous innovation in features like multi-currency clearing and credit integration paint a compelling picture of a future where UPI plays a pivotal role in shaping a more interconnected, efficient, and financially inclusive global economy.

You must be logged in to post a comment.